How coal turned from biggest asset to biggest risk for energy companies

September 13, 2021

Having cheap coal-fired generation in your electricity portfolio used to be one of the biggest competitive advantages for vertically integrated energy companies or “gentailers”. However, the role and value of baseload coal is quickly disappearing in Australia’s National Electricity Market (NEM), as the uptake of renewable energy grows. Companies with a heavy exposure to coal, such as AGL, will need to transition their business models if they want to survive.

Last week, I was invited to speak on this issue at the AGL Investor Briefing held by the Australasian Centre for Corporate Responsibility (ACCR). This article summarises some of the key takeaways.

Renewables squeezing out fossil fuels

Variable renewable energy (VRE) squeezing out fossil fuel generation has been the story of the last decade in the NEM (see chart below). Two big milestones have been reached in recent years:

1. 2017-18 was the first financial year where variable renewables generated more electricity than gas-fired generators. Furthermore, gas generation finished the 2020-21 financial year at the lowest level it has ever been.

2. 2019-20 was the first financial year where variable renewables generated more electricity than brown coal.

Note that in the chart above, VRE includes the electricity generated from wind power, large-scale solar, and rooftop solar.

Brown coal-fired generators need high capacity factors to remain economically viable and face increasing maintenance costs as they age. We have already seen a number of brown coal casualties, which have exited the market such as South Australia’s Playford B in 2012 and Northern in 2016, as well as Victoria’s Hazelwood power station in 2017.

So how exactly do renewables squeeze out fossil fuels? In the wholesale energy market, power stations submit bids stating how much electricity they are willing to supply and at what price. The market operator then dispatches the cheapest generators to meet the demand in the market. In contrast to fossil fuels, wind and solar do not have a fuel cost. Their marginal cost is essentially zero. As a result, they frequently bid $0/MWh for their electricity. This means that more expensive generation is pushed to the back of the dispatch queue. This is also the same mechanism by which renewables put downward pressure on wholesale prices. It is known as the “merit order effect”. Furthermore, as renewables put downward pressure on prices, this eats into the profits of inflexible generation such as coal, which runs through the low price periods.

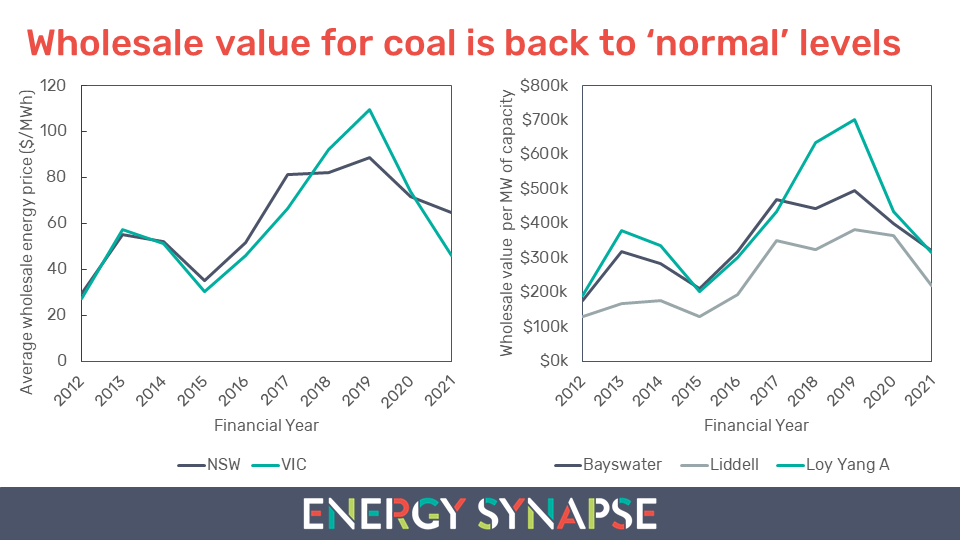

Wholesale value for coal is back to ‘normal’ levels after energy crisis super profits

The NEM experienced record high wholesale electricity prices during 2017-2020. This period was known as the “energy crisis”. The energy crisis was driven by several factors coming together such as high gas prices, snap exit of ageing generation such as Hazelwood, outdated market rules, a decade of energy policy uncertainty, and more. Unsurprisingly, power stations (including coal) earned record high revenues in the wholesale market during this time. However, these super profits were never going to be sustainable.

The chart below uses AGL’s portfolio of coal generators (Bayswater, Liddell and Loy Yang A) as an example. We have normalised the wholesale market value of these asset by their capacity in order to compare the value of power stations of different sizes. You will notice that Liddell is the least valuable asset from a $/MW perspective. It is also the first of AGL’s coal plants scheduled for retirement starting from April 2022. Liddell’s low value is driven by a very low capacity factor, which was just 42% in FY2020-21. In contrast, Bayswater (which is also in NSW) had an average capacity factor of 62%. Even this figure is the lowest capacity factor that Bayswater has had over the 10 year period depicted in the chart.

Note that Australia had a carbon price from July 2012 to June 2014. This increased wholesale prices and hence wholesale values, but fossil fuel generators also had to payout the carbon price, which is not depicted here. Thus, although the current wholesale values are significantly lower than the super profit era, the situation is not dire compared with historical averages. This is an important point. We are not suggesting that all coal-fired power stations need to close tomorrow. But rather that a 10 year closure plan is needed.

So what might the future for coal look like? South Australia can give us some good hints.

South Australia gives a preview of the changing paradigm

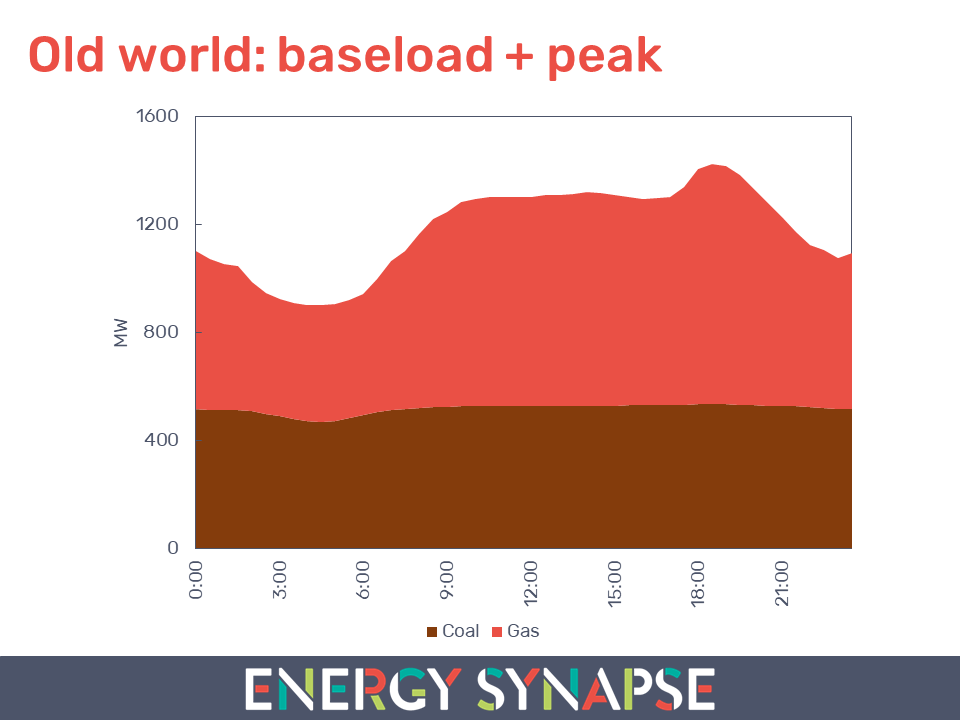

15 years ago, South Australia’s grid was dominated by coal and gas (see chart below). Coal fired power stations have high fixed costs, but low marginal costs. They are also slow to start and have relatively low ramping ability. This results in coal operating in a constant or “baseload” pattern.

In contrast, gas-fired generators have low fixed costs and much higher marginal costs. They are also quicker to start and have higher ramping capabilities. This results in gas generators operating as “peakers”.

There are of course variations within these categories. For example, black coal generators tend to be significantly more flexible than brown coal generators and hence we see black coal being better able to follow pricing patterns in the market.

Similarly, closed cycle gas turbines (CCGT) tend to be less flexible than other types of gas generators and hence traditionally served what was known as the “intermediate peak”.

However, the main point here is that the traditional paradigm of “baseload” and “peak” comes from the economic characteristics of these generators.

In order for the grid to remain stable, it is vital that the supply of electricity is in balance with the demand for electricity at every point in time. Baseload plus peak is one option for the supply side, but it is not the only option, and certainly not mandatory. It is important to recognise that baseload generation is a business model, not a technical requirement. That business model is what is in danger.

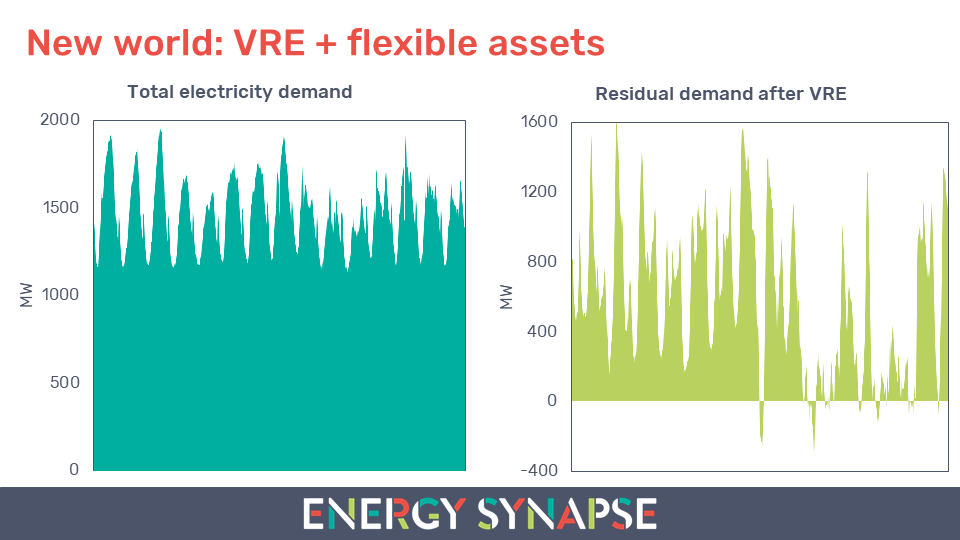

The chart below shows what South Australia looks like today. This data is from the first 15 days in April 2021. The figure on the left shows the electricity demand from consumers and businesses. There is nothing particularly unusual about this pattern. However, once you subtract rooftop solar, large-scale solar, and wind, you are left with the residual demand profile on the right.

As you can see, there is no “baseload” left for coal to serve. This is not a pattern that coal-fired generators are able to follow.

This residual demand is predominately being met by gas generators, and to a lesser extent, batteries. As other states ramp up their levels of wind and solar, we can expect this NEM wide residual demand pattern to be met by a portfolio of highly flexible assets including gas, batteries, hydro, and demand response. It will also be aided by improved interconnections between regions.

Coal, however, does not have a role in this new world. More importantly for investors, coal has little value in this new world. The most valuable energy assets in a highly renewable grid will be the ones that offer the most flexibility.

Furthermore, this is not something that the contracting market will be able to overcome. Industrial energy users have been the traditional offtakers for coal generators. However, these energy users are increasingly moving toward renewable supply to reduce costs and manage their own carbon risks. For example, Tomago Aluminium, the single biggest energy user on the grid, recently announced that they will move to predominately renewable supply when their current contract with AGL ends in the late 2020s.

Coal will struggle to remain economically viable beyond 2030

The pace of renewable energy installations, both utility-scale and behind-the-meter, continue to break records and exceed expectations. As of July 2021, there were almost 6 GW of committed large-scale clean energy projects in the NEM and a further 2 GW in mid-stage development. Astonishingly, there are over 110 GW of large-scale clean energy projects in early development. Of course, most of these projects will not proceed as they will be found to be unattractive during the feasibility stage. However, the sheer scale of projects under development is a good illustration of the looming threat for coal.

Our internal analysis has shown that coal-fired power stations will struggle to survive beyond 2030 without government support. Savvy energy companies will recognise this risk and the need to have a transition plan to exit coal within the 10 years. On the other hand, those that ignore the risks will find themselves in hot water very quickly.

Don’t bank on capacity mechanism to save coal

The Energy Security Board (ESB) has recently provided its final advice to Australia’s energy ministers as part of the post 2025 electricity market design project. The most controversial aspect of this advice relates to the introduction of a capacity mechanism (the Physical Retailer Reliability Obligation (PRRO)).

Many commentator’s first thought was that a capacity mechanism automatically equates to a subsidy to prolong the life of coal. Those heavily invested in coal should be very cautious about counting their chickens before they have hatch as this could very well be a double-edged sword for coal.

1. High uncertainty whether PRRO will actually go ahead

Firstly, the capacity mechanism is little more than a thought bubble at present. The ESB is seeking “in-principle support” from ministers and the go-ahead to develop a detailed design for the mechanism. This would then be put in front of ministers for approval by mid-2023.

“In-principle support” is very far removed from actual implementation. Even if the support is granted, the capacity mechanism could very well fall over during the design stage. It will be subject to substantial stakeholder consultation, and most industry players have already voiced strong opposition to capacity mechanisms.

2. Implementation unlikely before 2025

Even if the eventual design is approved, market participants would need to be given adequate notice before a major reform like the PRRO goes live. This makes practical implementation unlikely before 2025. For energy companies who elect a “wait and see” approach, this will be a long time to lose without a transition strategy in place.

3. PRRO design could actually backfire on coal

The design of the mechanism is still very much a blank slate. This means that there is a real risk that the eventual design could actually disadvantage rather than favour coal. For example, the capacity mechanism could be structured such that higher payments are made to faster responding and more flexible assets. These are traits that the ESB has already flagged that it wants to reward. The mechanism could also be structured to include an emissions intensity threshold, which could disadvantage or even completely exclude coal. The former point has not been explicitly raised by the ESB, but it could be a real possibility, especially if there is an change in federal government in the next or subsequent elections.

The capacity mechanism is simply too uncertain to be relied upon as a saving grace for coal. The transition to clean energy is a threat to traditional energy businesses. But it also presents a once in a lifetime opportunity to reap the rewards from developing a future proof business model that aligns market opportunity with customer and shareholder values. Regardless of the PRRO, the time to plan for coal closures is still now.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter