AEMO’s Draft 2026 ISP: Extended coal timelines and strategic implications for developers

December 11, 2025

AEMO released its Draft 2026 Integrated System Plan (ISP) on 10 December 2025. The ISP charts Australia’s energy infrastructure needs through to 2050. For developers of utility-scale renewable energy and storage projects, this roadmap presents both significant opportunities and a sobering recalibration of coal retirement expectations.

Scale of opportunity

The Draft 2026 ISP‘s optimal development path calls for massive deployment of renewable energy and storage. By FY 2050, the National Electricity Market (NEM) requires 120 GW of utility-scale wind and solar and 32 GW of utility-scale storage. This represents a fundamental reshaping of Australia’s generation landscape.

Near-term targets are aggressive: 27 GW of utility-scale storage by 2030. This timeline demands immediate action from developers who can bring storage projects to market.

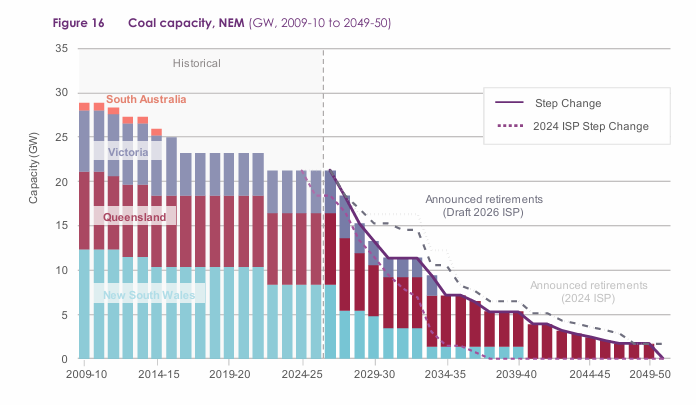

Draft 2026 ISP slows down coal closures

For clean energy developers, understanding coal closure timing is critical because it defines when and where replacement capacity becomes economically viable. The Draft 2026 ISP marks a significant coal closure slowdown compared with the previous ISP published in 2024.

Under the 2024 ISP Step Change scenario, coal exited the market completely by FY 2038. In contrast, the Draft 2026 ISP Step Change scenario retains coal until FY 2049. This adjusted timeline reflects the intent of the Queensland Energy Roadmap (read our analysis on QLD policy for more details) as well as slower than previously planned closures in NSW and Victoria.

A slower coal retirement trajectory creates complex implications for developers:

- Reduced near-term urgency for long duration storage: The extended timeline reduces immediate pressure for replacement long duration capacity. Projects banking on coal retirement creating capacity scarcity may face delayed market signals or weakened business cases in the 2030-2040 period.

- Extended fossil fuel competition: Coal generation remains a price-setting competitor for longer. A large portion of coal generation is a “must run” resource due to its operational inflexibility, and hence frequently bids low or even negative prices in the energy market. This could suppress wholesale electricity prices during periods of coal operation, potentially impacting returns from solar and wind projects. Developers must model scenarios where coal persists longer than previous plans suggested.

- Reliability risk increases: Reliability could be at risk as the coal fleet ages. When units fail unexpectedly, market volatility spikes, benefiting projects with flexible capacity, such as batteries.

Whether coal will even be capable of operating into the late 2040s is highly questionable. AEMO acknowledges that coal may retire faster than their forecasts due to rising operating costs, reduced fuel security, high maintenance costs, and greater competition from renewable energy, all eroding financial viability. Developers must navigate this ambiguity when making long-term investment decisions.

From a policy and regulatory perspective, it will be critical to increase the speed at which renewable/storage projects are able to progress through the development process and reach financial close. A faster build pace is essential for managing risks associated with earlier coal closures and/or declining coal reliability.

Electricity usage to almost double

The ISP anticipates an almost doubling of underlying electricity consumption from 205 TWh today to 389 TWh by FY 2050. Key drivers of growth include transport electrification, data centre expansion, and industrial gas-to-electricity switching.

Consumer-side adoption is expected to accelerate alongside grid-scale deployment. The plan anticipates 87 GW of rooftop solar supported by 27 GW of behind-the-meter batteries, of which 53% would participate in a virtual power plant (VPP). The Draft 2026 ISP Step Change scenario also forecasts 80% of all vehicles to be electric (EVs), with 11% participating in vehicle-to-grid (V2G) programs to provide an additional 9 GW of coordinated storage. This growth in consumer energy resources (CER) creates both competition and complementary opportunities for utility-scale projects.

Transmission reduced, but still essential

The Draft 2026 ISP requires 6,000 km of new transmission lines to be added to the existing 44,000 km network. The overall extent of new transmission has reduced compared to the previous ISP, with some projects being downsized or no longer needed in response to policy or other changes (1,350 km), and others being removed from the total as they have progressed to operation (365 km).

Gaining investment certainty

The energy transition depends on timely investment decisions, which are hampered by uncertainty. There are a number of policy mechanisms that can help derisk some of the uncertainty that comes with investing in a system in transition. This includes the federal Capacity Investment Scheme (CIS), Long-Term Energy Service Agreements (LTESAs) in NSW, Firm Energy Reliability Mechanism (FERM) in South Australia and the NEM Wholesale Market Settings Review currently under consideration.

Developers will also find it helpful to stress test different market scenarios (e.g. pace of coal closures) through modelling to understand the revenue impact on their projects.

Energy Synapse specialises in market and revenue modelling for utility-scale renewable energy and storage projects. Learn more about our approach.