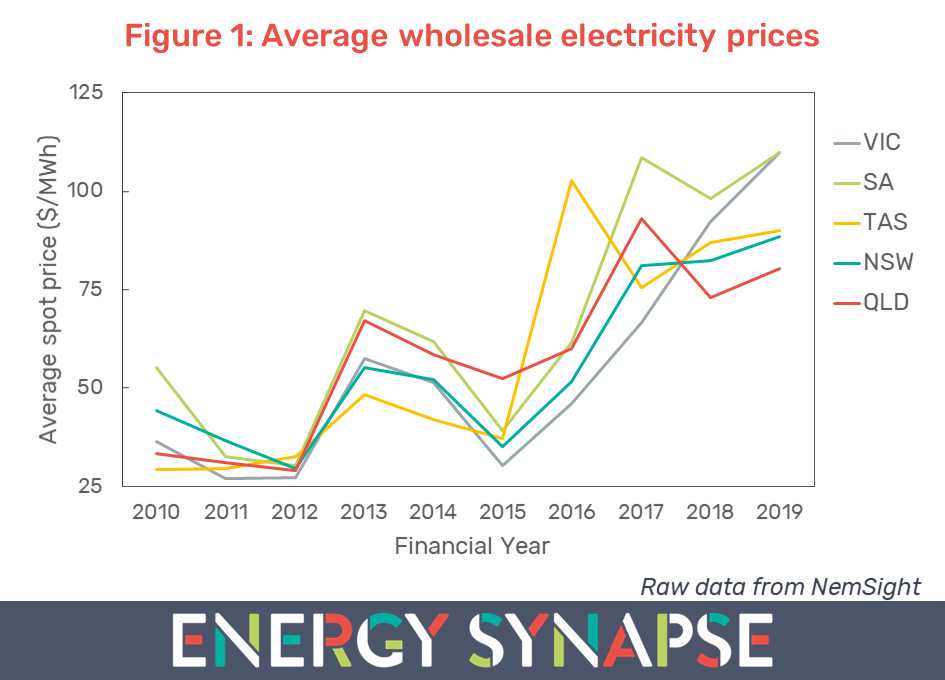

Financial year ending June 2019 saw wholesale electricity prices rise in every state in the National Electricity Market (NEM). Victoria had the highest increase on the previous financial year at 19%, followed by South Australia (12%), Queensland (10%), New South Wales (8%), and Tasmania (3%) (see Figure 1). This data has been compiled using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Wholesale electricity prices have tripled over the past decade in Victoria and Tasmania and have doubled in Queensland, NSW, and South Australia. This energy crisis has been brought about by a combination of factors coming together. These include high gas prices, a decade of policy uncertainty, exit of ageing generation, lack of competition, outdated market rules, and more. And it is still very much on-going. Prices in South Australia, Victoria, and NSW all reached record highs in the 2019 financial year.

Pricing in Tasmania peaked earlier in FY 2016, due to a prolonged outage of the Basslink interconnector, which links to the mainland grid.

Queensland peaked in FY 2017. In mid 2017, the Queensland Government directed state owned generators to alter their bidding practices and put downward pressure on wholesale electricity prices. This direction has been one of the main reasons why Queensland has had the lowest wholesale electricity prices in the NEM for the last two years, despite growing max demand. However, this bidding direction ended on 30 June 2019. It will be interesting to see whether the bidding behaviour from state owned generators reverts back to old patterns over the coming summer.

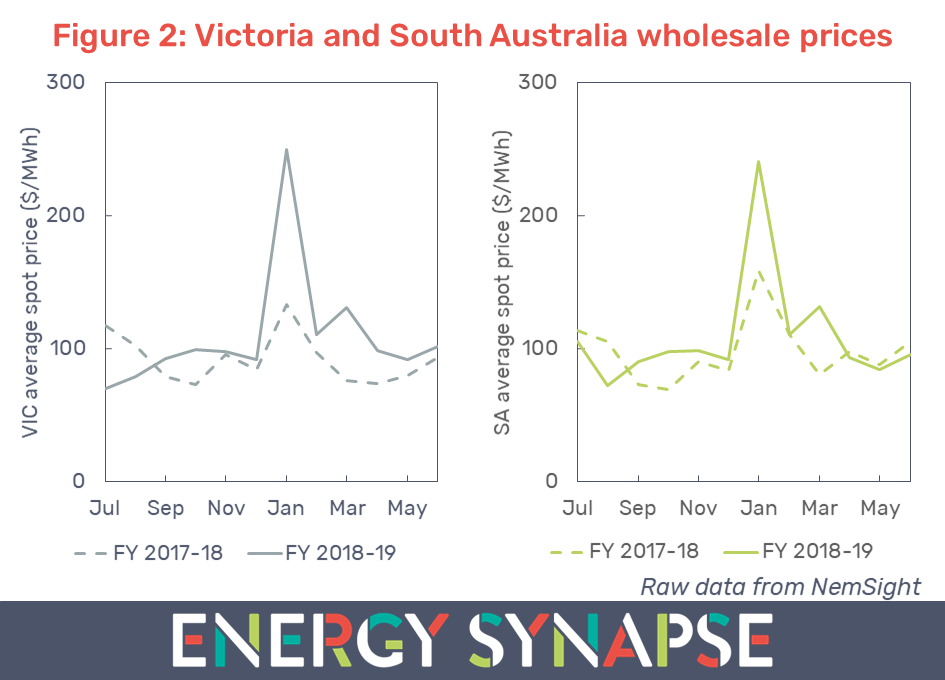

Victoria and South Australia battled record heat and coal failures

High summer prices drove the annual price increase in Victoria and South Australia as seen in Figure 2. This was largely weather related as Australia sweltered through the hottest summer on record.

However, it was also due to multiple failures at Victorian coal-fired power stations, particularly on the 24th and 25th of January. An extreme heatwave gripped South Australia and Victoria, with some regions experiencing record high temperatures. Multiple brown coal outages led to 1.1 GW of thermal generation being unavailable on 24 January and 1.6 GW being unavailable on 25 January (see report by AEMO). This created a shortage of supply, with the unfortunate result of load shedding in Victoria and record high electricity prices.

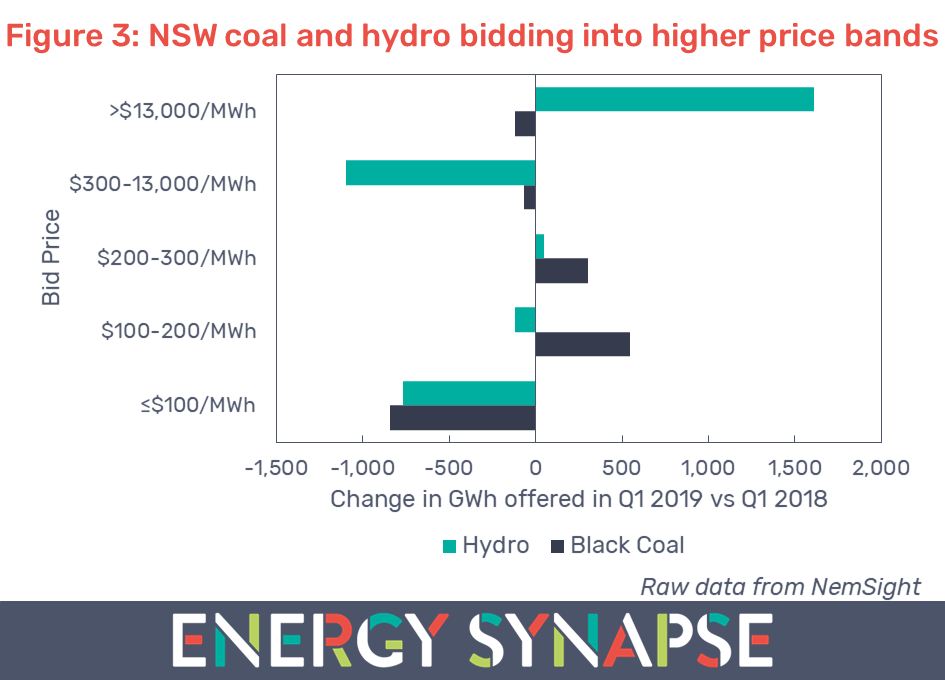

NSW coal and hydro generators raised bids

In contrast to Victoria and South Australia, pricing in NSW was not particularly volatile. The main contributing factor to higher prices was a change in bidding behaviour from coal and hydro generators during the first quarter (Jan to Mar) of 2019.

Figure 3 shows that black coal generators reduced the amount of electricity they offered in price bands ≤$100/MWh and instead bid this energy into higher price bands between $100/MWh and $300/MWh.

The change in bidding behaviour was even more drastic for hydro generators, who significantly cut bids in the ≤$100/MWh and $300-13,000/MWh price bands and instead bid this energy at prices greater than $13,000/MWh. Dry conditions and low storage levels were contributing factors.

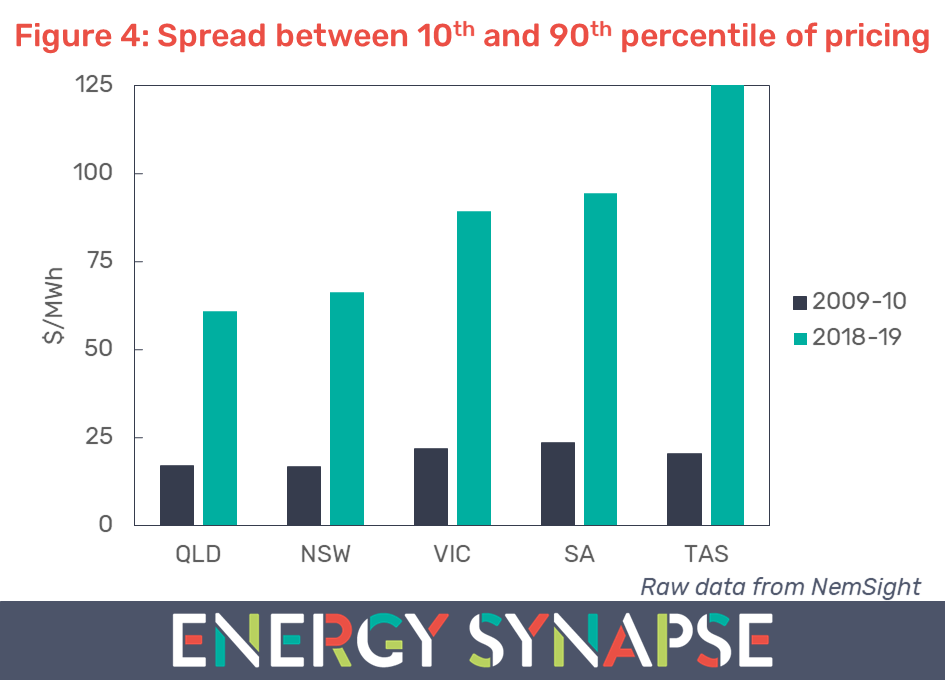

Spreads in wholesale electricity prices on the rise

Another interesting trend over the past decade has been the growing spread (or difference) between the 10th and 90th percentile of pricing. This has interesting implications for energy storage, which is most economic when spreads are high.

Figure 4 shows the spread for each region in the NEM in the last financial year versus 10 years prior. Ten years ago, spreads very were small, varying between $17-24/MWh across states. This offered limited arbitrage opportunities in the spot market. In contrast, in the last financial year, spreads ranged from $60/MWh to $125/MWh. As an example, the Tesla big battery in South Australia achieved an average price differential of $76/MWh (inclusive of round trip efficiency losses).

As more zero marginal cost renewable energy enters the market, we can expect wholesale prices to keep decreasing at the times when renewables are generating power.

Queensland gave the perfect example earlier this week when daytime prices hit zero/negative for a record nine consecutive days. This was predominantly due to high solar uptake, low electricity demand, and inflexible coal. RenewEconomy covered some of our commentary here and here.

In contrast, when renewable energy is less available, prices tend to go up. The opening up of spreads is a predictable outcome of the transition to renewable energy. It will be largely up to energy storage, as well as demand response, to regulate spreads going forward.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter

National Electricity Market year in review part 2/2: Changing energy mix

January 18, 2019

Share

In the second installment of our National Electricity Market (NEM) Year in Review series, we will be looking at how the energy mix has evolved over the past year.

If you missed part one, we examined the major events that shaped wholesale electricity prices during 2018.

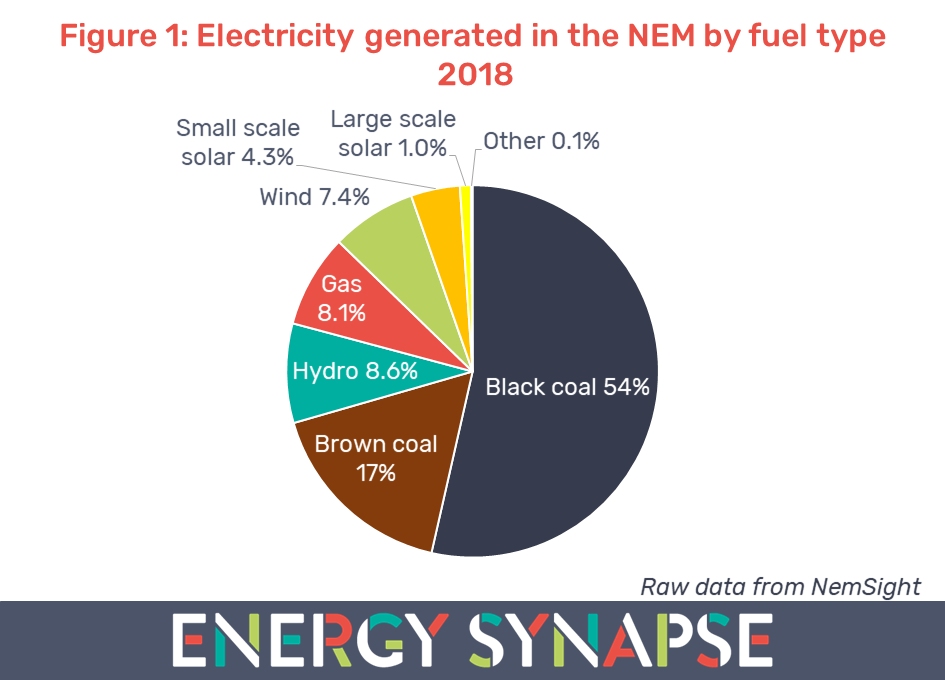

Figure 1 shows the percentage of electricity generated in the NEM by each fuel type. This data has been compiled using NemSight, a software developed by Creative Analytics (part of the Energy One group). Note that we have included generation from small scale solar (≤ 100 kW) as it is increasingly becoming a significant source of power in the NEM. But strictly speaking, rooftop solar is treated as negative demand rather than generation.

During 2018, electricity generated from variable renewable energy (wind, small scale solar, and large scale solar) accounted for 12.6% of total electricity generation in the NEM. This is approximately a 30% increase on 2017, when variable renewables represented 9.8% of generation. Fossil fuels, and in particular coal, still dominate generation in the NEM, accounting for almost 80% of all generation.

Exponential growth in large scale solar

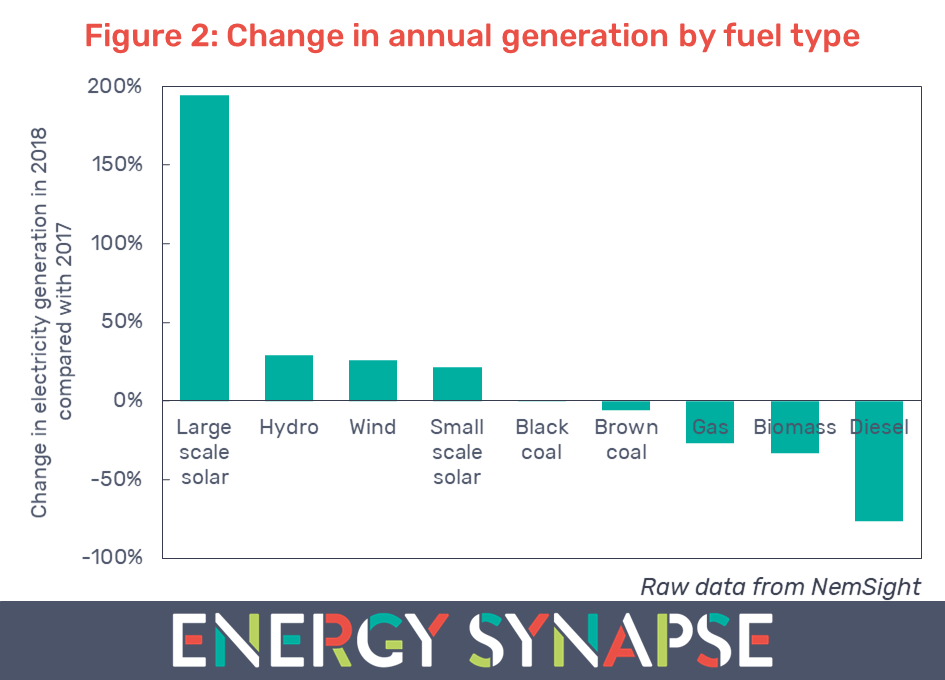

Figure 2 shows the percentage change in electricity generation for each fuel type in 2018 compared with 2017. The data in both Figures 1 and 2 is based on GWh generated rather than capacity. As can be seen in Figure 2, 2018 was the year of large scale solar. Generation from large scale solar almost tripled in 2018, completely eclipsing the growth in any other fuel type.

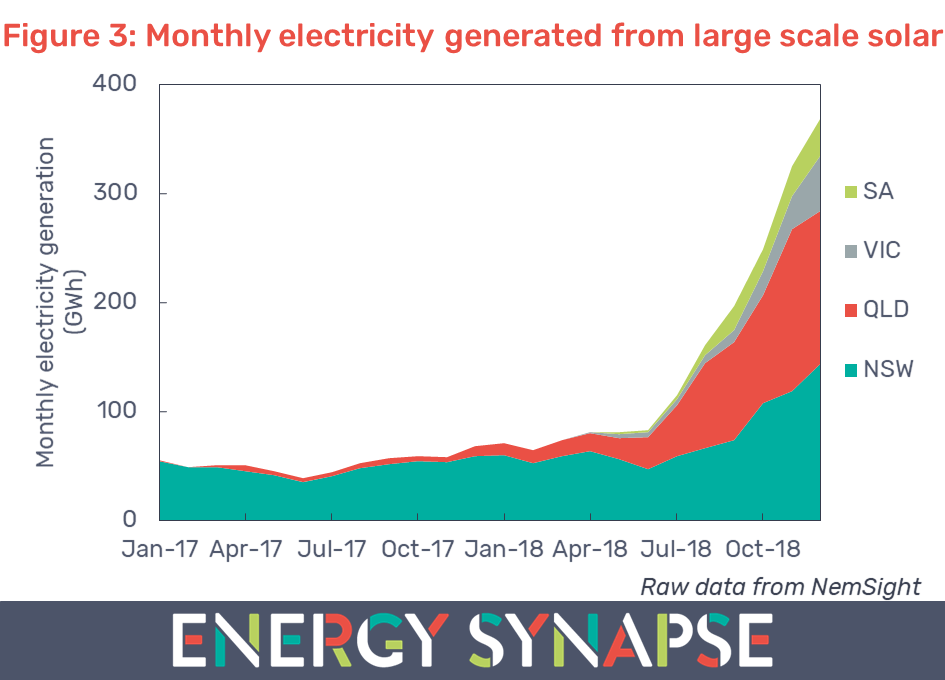

Large scale solar still only represents a very small portion (1%) of NEM generation. However, it has experienced extraordinary growth in the second half of 2018, as new capacity has come online (see Figure 3). The biggest growth has been in Queensland. In 2018, the electricity generated from large solar in Queensland was more than 14 times higher than in 2017.

Small scale solar has also seen strong growth, with the generation from these systems increasing by 21% in the NEM (see Figure 2). Queensland leads the nation in terms of both installed capacity of small solar (2220 MW) as well as having the highest percentage of dwellings with solar PV (33%) (Source: APVI). Furthermore, the statistics for 2018 will continue to grow as more systems are officially registered over the next 12 months.

The high growth in solar (both large and small scale) is already having a profound effect on wholesale electricity prices. In a previous article, we used Queensland as a case study to demonstrate how solar is pushing down daytime wholesale electricity prices. We are seeing daytime prices fall out of the top quartile of pricing and into the bottom quartile. This has big implications for developers of future solar projects, as they may see returns diminish.

Renewables (including hydro) are displacing higher priced gas generation

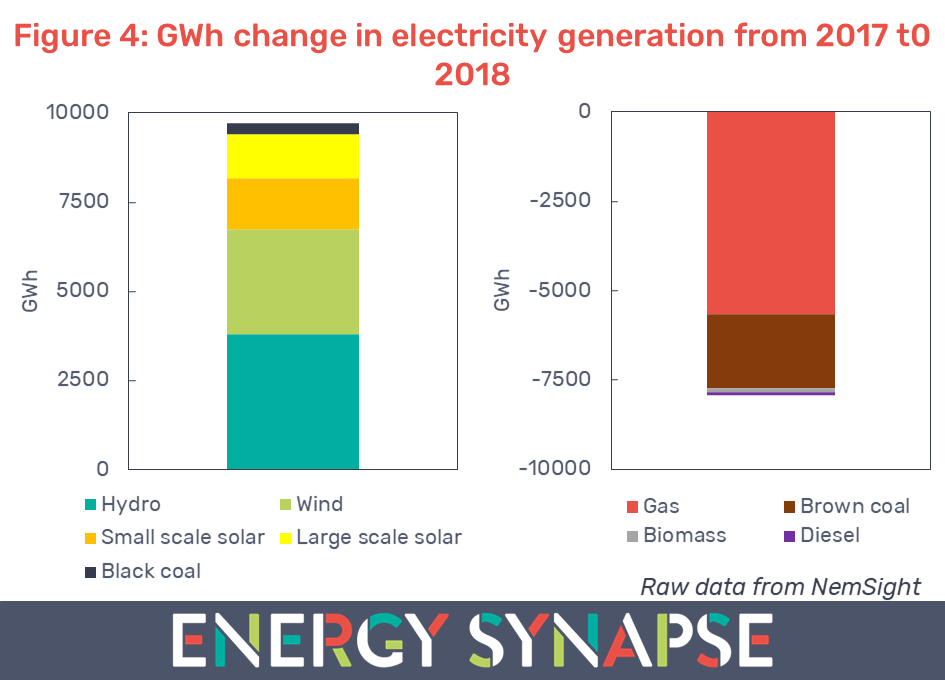

Figure 4 shows the change in electricity generation by each fuel type, but this time as a GWh change rather than percentage. The left hand side shows the fuel types that had an increase in generation. The right hand side shows the fuel types that had a decrease in generation. The difference between the two charts (approximately 1800 GWh) is the load growth in the NEM.

We can see that in absolute terms, gas generation was the biggest loser in the energy mix in 2018. Electricity from gas decreased by 5660 GWh (27%) across the NEM as a whole. The overall capacity factor for gas generation fell to just 16.6%, compared with 22.6% in 2017. There are several reasons for the reduction in gas generation:

1. Gas generation was less available throughout 2018.

2. The gas generation that was available, was bid in at higher prices to reflect the higher pricing in gas markets.

3. Existing hydro generation, especially in Tasmania, offered its capacity at much lower prices as we explained in part one. This is the main reason for the growth in hydro’s capacity factor from 17.3% in 2017 to 22.3% in 2018.

4. Wind and solar have a zero marginal cost and hence tend to bid into the wholesale market at ≤ $0/MWh. This means they are at the very bottom of the bid stack. The growth in renewables combined with hydro offering lower prices, meant that any available gas was increasingly squeezed out of the market.

Brown coal decreasing with closure of Hazelwood

Hazelwood, a 1600 MW brown coal fired power station in Victoria, was closed at the end of March 2017. As a result, brown coal generation fell by 18% in 2017 compared with 2016, and again by 6% in 2018.

Following the closure, existing coal fired power stations have picked up some of the slack. Even though total coal generation is down, the capacity factor for brown coal has increased from 72% in 2016 to 81% in 2018. The capacity factor for black coal has also increased from 61% in 2016 to 65% in 2018.

As more ageing fossil fuel generation exits the market, and more renewable energy comes online, we can expect the energy mix to keep evolving. Stay tuned for part three of our series…

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter