CIS tender analysis: project configuration and success patterns

March 5, 2026

Analysis of almost 400 bids submitted across completed Capacity Investment Scheme (CIS) tenders in the National Electricity Market reveals clear patterns in project configuration and competitive positioning. 61 projects have been awarded to date, which represents a 15% success rate. Understanding these trends is essential for developers planning submissions in upcoming tender rounds.

This analysis examines the first three NEM tenders, plus the SA-VIC pilot tender, to identify market signals that are shaping investment decisions in utility-scale renewables and storage.

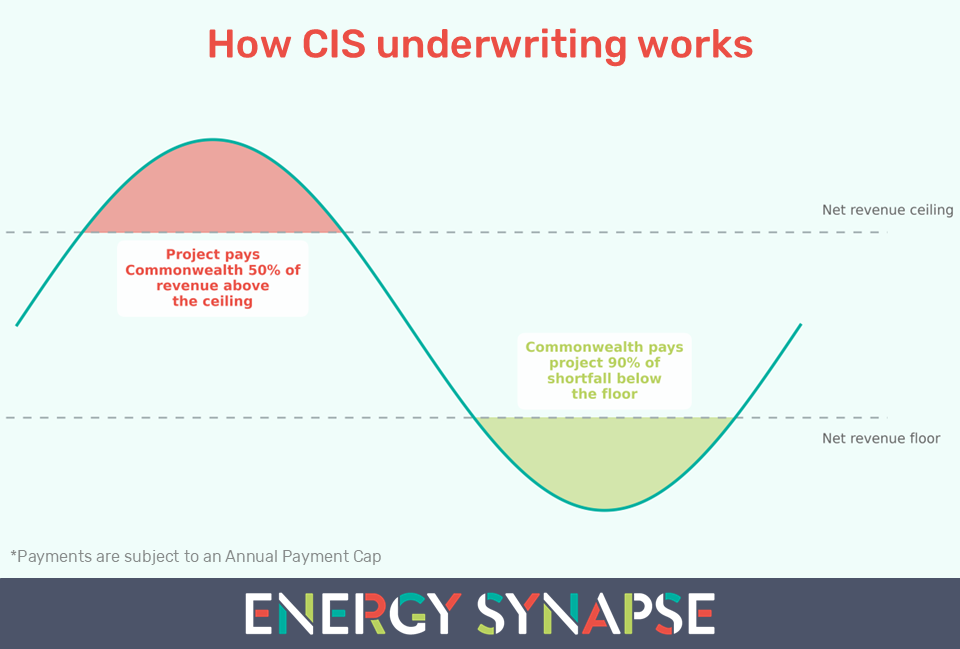

The CIS is the Australian Government’s primary mechanism for underwriting investment in large-scale renewable generation and clean dispatchable capacity. The CIS provides revenue support through a cap-and-collar framework rather than fixed subsidies. This structure maintains project exposure to market signals while reducing downside risk for investors.

Competitive dynamics across NEM CIS tenders

Success rates by tender

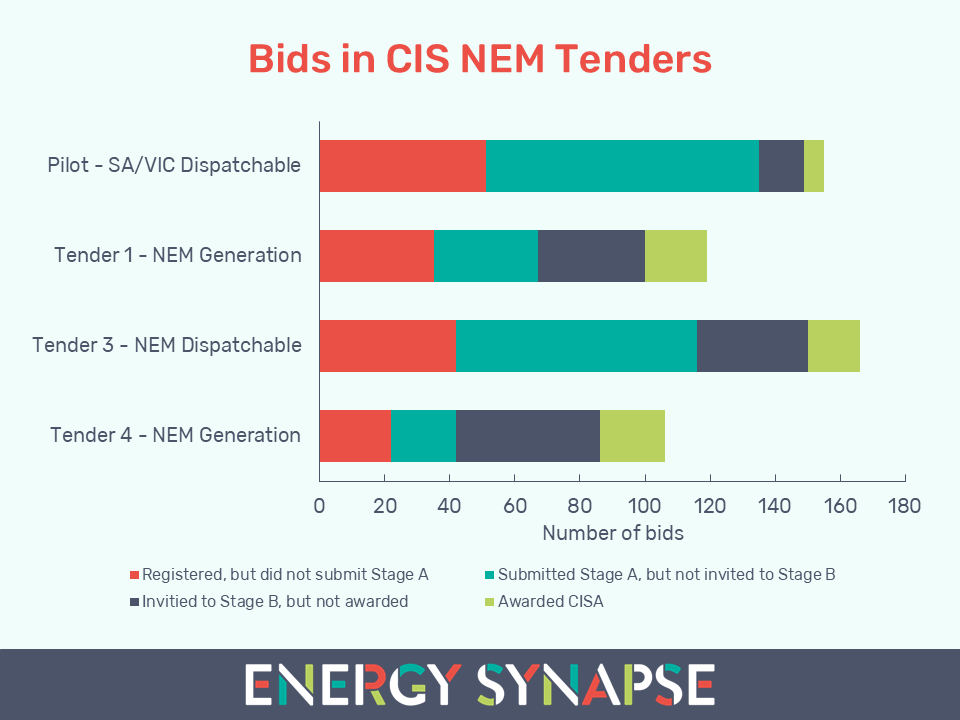

CIS tenders have consistently attracted strong competition, with aggregate bid capacity significantly exceeding tender targets. This oversubscription reflects both the commercial value of revenue underwriting in the current market environment and the depth of Australia’s clean energy project pipeline.

Across the three formal NEM tenders and SA/VIC pilot tender, a total of 396 bids were submitted to Stage A, with 61 projects being awarded a Capacity Investment Scheme Agreement (CISA). This 15% success rate demonstrates the selective nature of the assessment process and the importance of strong technical, financial, and social license credentials.

Note on data scope: This analysis excludes the Joint CIS NSW pilot tender, which was integrated with the NSW LTESA program and operated under different parameters. Data is drawn from publicly available DCCEEW tender outcomes and assessment summaries.

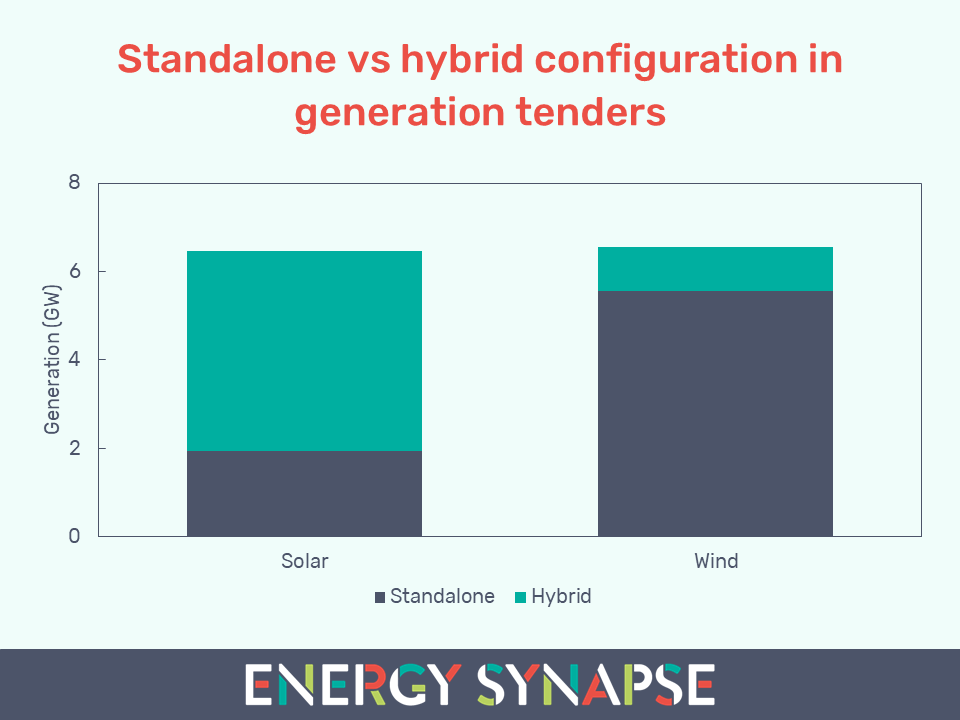

Hybrids in generation tenders

Wind and solar projects have been awarded similar capacities in generation tenders. However, there are significant differences in project configuration.

70% of awarded solar capacity was in hybrid configuration with battery storage, with only 30% of solar capacity being awarded in standalone configuration. This reflects a broader developer response to declining daytime wholesale energy prices. Hybridisation with battery storage allows developers to shift generation to higher value periods (e.g. evening and morning), strengthening both revenue profiles and system reliability contributions.

Wind generation shows a different pattern, with 85% of awarded capacity in standalone configuration and 15% in wind/BESS hybrids. However, interest in wind/BESS hybrids has grown substantially through 2025. Future tenders may see higher wind/BESS penetration as developers seek to maximise site value and provide flexible capacity.

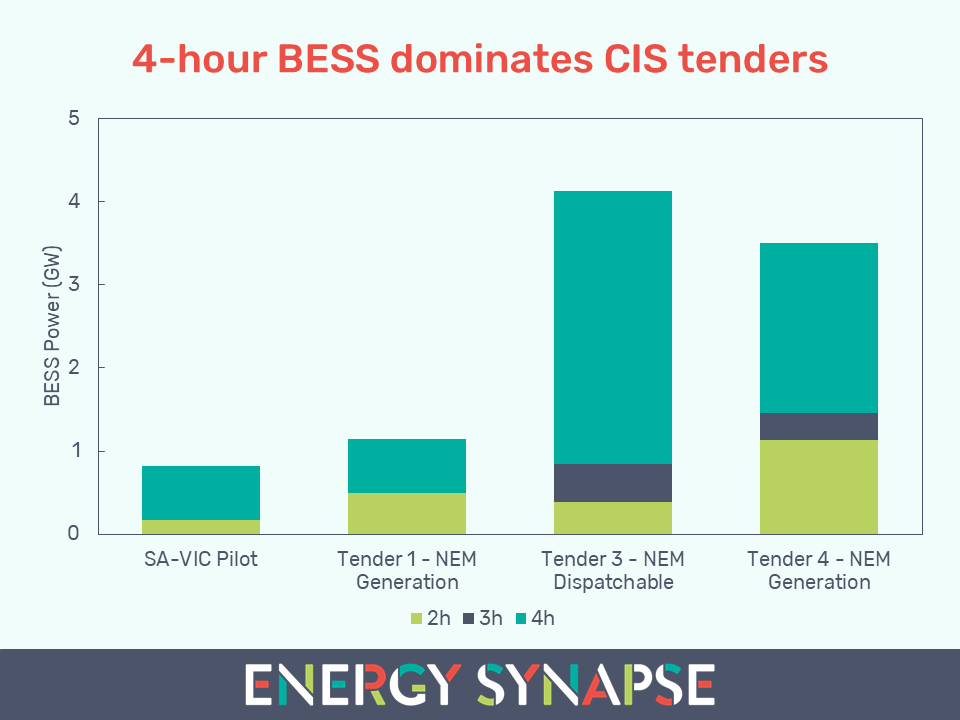

4-hour storage emerges as baseline

While CIS tender guidelines specify a minimum two-hour duration requirement for dispatchable capacity, awarded projects have consistently skewed toward four-hour configurations. This trend was most evident in Tender 3, the dedicated dispatchable capacity round, where 80% of awarded BESS capacity had approximately four hours of storage.

The preference for 4-hour duration indicates that assessment criteria weight both peak capacity and extended firming capability. Projects offering only 2-hour duration appear less competitive for standalone dispatchable CISAs, though shorter-duration storage remains viable in hybrid configurations where the primary capacity is renewable generation.

Implications for upcoming CIS tenders

CIS tenders are continuing to run every 6-months through to 2027 via a more streamlined single-stage application process. Competition for remaining capacity will likely intensify as the program approaches its target.

For solar developers: The data suggests standalone solar faces increasingly difficult competitive dynamics in the CIS. Developers should evaluate whether hybrid configuration strengthens their value proposition across merit criteria, particularly system reliability contribution, which weighs heavily in assessments.

For storage developers: Four-hour duration has emerged as the competitive baseline for dispatchable CISAs. Projects with shorter duration should articulate clear value differentiation, or consider positioning as hybrid components rather than standalone dispatchable assets.

For wind developers: While standalone wind has seen success to date, the economic case for wind/BESS hybrids is strengthening. Developers with suitable sites should assess whether storage addition improves both revenue modelling outcomes and competitive positioning in future tenders.

How Energy Synapse can help

Energy Synapse provides specialised analytical support for developers participating in CIS tenders, including:

- Revenue modelling under CISA cap-and-collar frameworks

- Market price forecasting and scenario analysis

- Optimal project configuration assessment

Contact our team to discuss how we can support your CIS tender preparation or broader development strategy.

Energy Synapse also offers an analytics platform that provides comprehensive tracking of power projects under development across the NEM, including CIS and LTESA underwriting status, REZ access rights, and development stage progression. Request a demo to see how the Energy Synapse Platform supports project development and strategic planning.