Developer’s guide to NSW long-duration storage LTESA

February 10, 2026

The long duration storage Long-Term Energy Service Agreement (LTESA) framework is the primary mechanism for de-risking 8+ hour storage investments in NSW, as the state transitions away from coal.

The NSW Electricity Roadmap has a target to reach a minimum of 2 GW/16 GWh of long duration storage by 2030, and 28 GWh by 2034. ASL’s 2025 Infrastructure Investment Objectives Report identified a development pathway that requires over 42 GWh of long-duration storage by 2034, which significantly exceeds the minimum objective.

For developers navigating this landscape, understanding the commercial structure and competitive dynamics of long duration storage LTESAs is essential to successful project development.

Understanding the LTESA mechanism

Unlike traditional contracts-for-difference, LTESAs provide revenue support through a series of options rather than guaranteed payments. Furthermore, LTESAs give projects flexibility to utilise market offtakes to manage their own price risks.

Different types of LTESAs include:

- Generation LTESA for wind and solar.

- Firming LTESA for dispatchable capacity such as batteries, electrolysers or gas generators.

- Long duration storage LTESA for 8+ hour storage.

NSW was the first state in Australia to develop an underwriting framework specifically for long-duration storage, which has a vital role in grid reliability as coal power stations retire. The long duration storage (LDS) LTESA is the focus of this analysis.

Option structure and exercise requirements

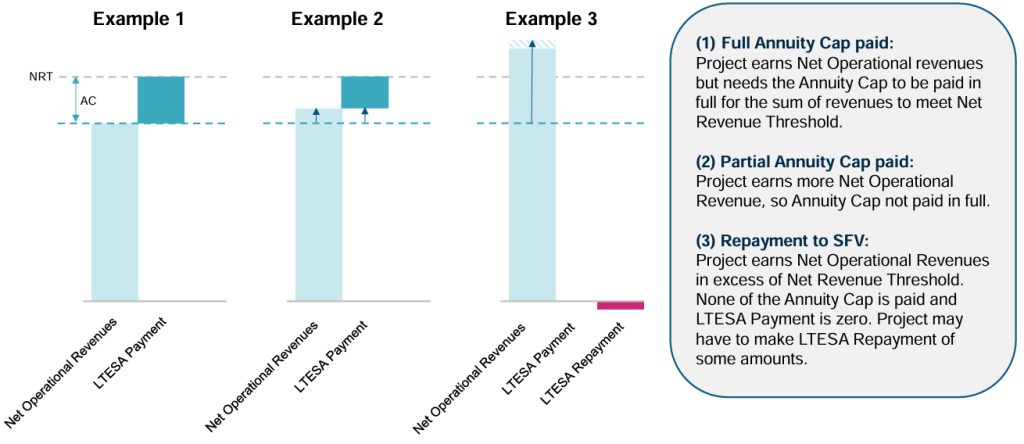

LDS projects receive a series of options to access a variable annuity payment in the form of a top up to net operational revenues. To exercise an option, operators must provide 6-12 months advance notice before the start of each financial year annuity period (1 July – 30 June).

This structure allows projects to opt out of support during periods when they expect strong merchant revenue. However, it also requires careful forward market assessment, which carries risk.

Payment calculation

When an option is exercised, the annuity payment is calculated as the lesser of:

- Annuity Cap (maximum annual payment, bid by the developer), or

- Annuity Cap – 75% × (Net Operational Revenue – (Net Revenue Threshold – Annuity Cap))

This formula creates a progressive reduction in support as project revenues increase.

Both the Annuity Cap and Net Revenue Threshold escalate annually at the lesser of CPI or 3%.

Repayment mechanism

Projects achieving revenues above the Net Revenue Threshold enter a benefit-sharing phase. The project operator repays 50% of revenues exceeding the threshold, capped at 100% of cumulative net payments received from the Scheme Financial Vehicle (SFV). This mechanism ensures NSW electricity customers benefit from upside scenarios while maintaining project incentives.

Source: AEMO Services Tender Round 6: LDS LTESA Proponent webinar

LTESA contract term

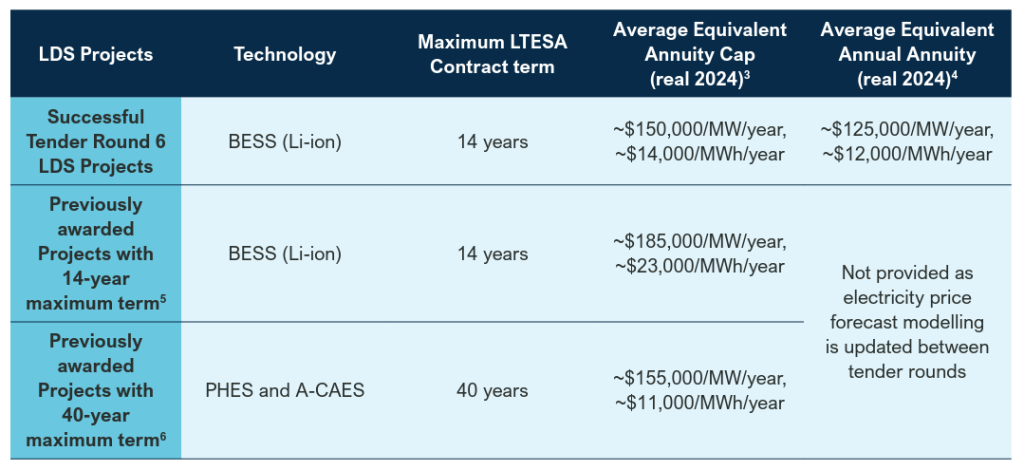

Contract terms vary by technology, with battery storage receiving terms up to 14-years, while pumped hydro projects can access the full 40-year maximum.

Insights on long duration storage LTESA winners

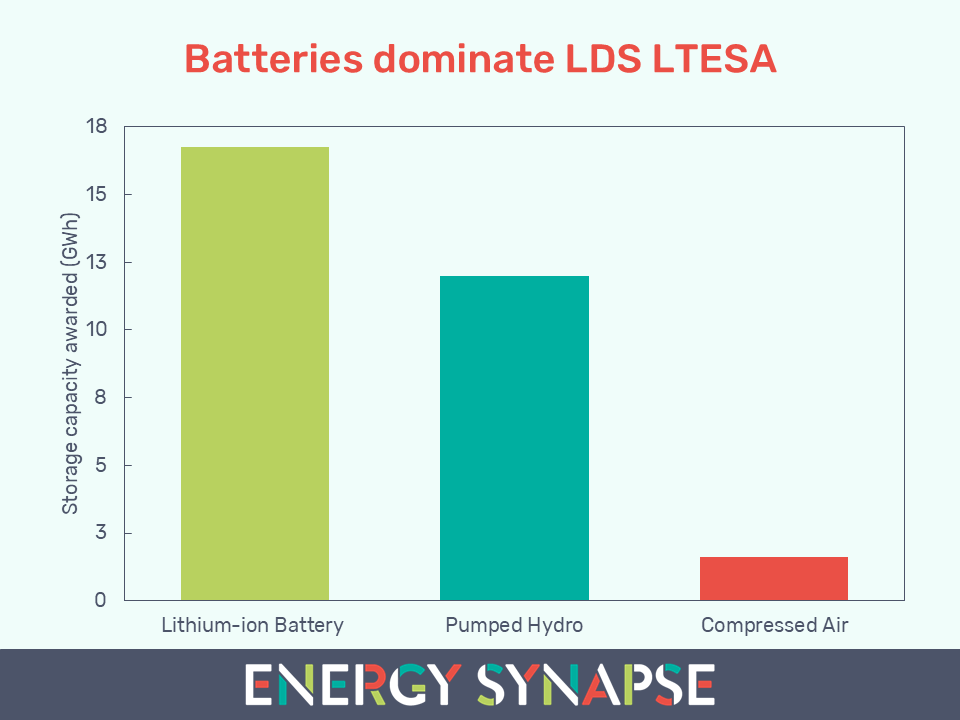

Six NSW Roadmap tenders have been completed to date, four of which have awarded long duration storage LTESAs (Tender 1, Tender 3, Tender 5, and Tender 6). 13 projects have been awarded long-duration LTESA’s representing a total of representing 2,770 MW and 30,362 MWh.

Lithium-ion batteries are the dominant technology

Lithium-ion batteries have been the dominant technology, representing 11 out of 13 successful projects and 16,722 MWh of storage capacity (55% of total awarded). This reflects the advantages of lithium-ion batteries in cost-competitiveness, bankability, supply chain maturity, and construction timeline certainty compared with other LDS technologies.

Only two non-battery projects have been successful in winning a LDS LTESA:

- Hydrostor’s 200 MW/1600 MWh Silver City Energy Storage project, which uses advanced compressed air energy storage, awarded in Tender 3; and

- ACEN’s 800 MW/11,990 MWh Phoenix Pumped Hydro project, awarded in Tender 5.

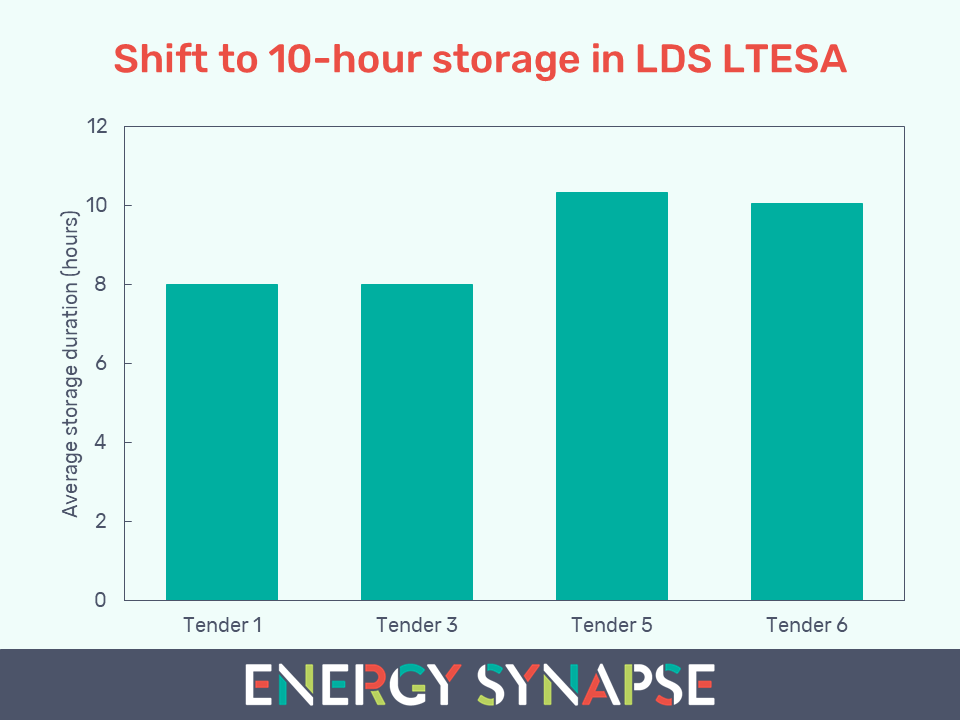

Shift to 10-hour storage

A clear evolution is evident in storage duration profiles. Rounds 1 and 3 delivered baseline 8-hour systems, meeting minimum eligibility requirements. From Round 5 forward, average duration has increased to approximately 10 hours. Longer durations have been assessed more favourably due to their potential to enhance both wholesale market benefits and system reliability contribution, which are key drivers of Merit Criteria 5 scores.

Network location is a key value driver

Being located in a strong part of the network with demonstrated flow capacity during peak demand has scored more favourably on Wholesale Market Benefits and System Benefits, compared with projects that are in more constrained parts of the network. ASL has indicated that good network location may be seen as more valuable than just adding storage capacity (MWh) to your project.

Structuring your LTESA bid for price competitiveness

In Market Briefing Notes, ASL has revealed that successful proponents have been structuring their bids in a way that lowers the potential Net LTESA Cost outcomes for NSW electricity customers. This can include:

- Low Annuity Cap: The Annuity Cap is the key pricing variable, and a competitively bid Annuity Cap minimises both Net LTESA Cost and Maximum Liability. Successful proponents set their Annuity Caps below their Net Revenue Thresholds, indicating they are accepting some market revenue risk and not relying on the LTESA to fully cover their investment costs.

- Reducing the contract term: A proponent may reduce the contract term or exclude Annuity Periods if they forecast sufficiently high operational revenue for those periods. This reduces the numbers of periods in which the Scheme Financial Vehicle (SFV) may be required to make top up payment and lowers potential LTESA cost outcomes for NSW electricity consumers compared to a full contract term.

- Taking on CPI risk: This reduces SPV’s cost exposure.

Round 6 demonstrated significant price compression. The Average Equivalent Annuity Cap for successful projects was approximately $150,000/MW/year (~$14,000/MWh/year in real 2024 dollars).

This represents a substantial reduction from Round 5, where lithium-ion projects averaged approximately $185,000/MW/year (~$23,000/MWh/year). This reflects maturing supply chains, increased developer confidence in merchant revenue, and intensifying competition.

Source: ASL Market Briefing Note on outcomes of Tender Round 6 for Long Duration Storage infrastructure

Source: ASL Market Briefing Note on outcomes of Tender Round 6 for Long Duration Storage infrastructure

Looking ahead to next LDS LTESA tender

The next LDS tender is expected to launch in Q2 2026 with an indicative target of 12 GWh. For developers, success requires not only understanding the LTESA mechanism but also positioning projects to maximise wholesale market benefits, system reliability contributions, and overall financial competitiveness.

Tender Round 6 pricing outcomes suggest the market is approaching a competitive equilibrium where only the most efficient, well-located, and strategically structured projects will succeed. Developers should focus on:

- Optimising project configuration (duration, capacity) for both technical performance and financial competitiveness.

- Developing sophisticated merchant revenue models to inform aggressive but credible bid structures.

- Securing connection agreements early to de-risk development timelines.

- Understanding network constraints and targeting high-value connection locations.

Energy Synapse provides market modelling, revenue modelling, and strategic advisory services to storage developers navigating the NSW Electricity Infrastructure Roadmap and LTESA tender processes. Contact us to schedule an introductory meeting with our team.