ESEM explained: How the Nelson Review improves bankability for renewables and storage

January 20, 2026

The National Electricity Market Wholesale Market Settings Review final report marks a defining moment for Australia’s energy transition. Led by Associate Professor Tim Nelson, the independent panel has delivered a comprehensive reform package that preserves the energy-only market while addressing critical barriers to investment in firmed renewable generation and storage.

With almost 70% of coal capacity expected to exit by 2038 and the Capacity Investment Scheme (CIS) concluding in 2027, these reforms arrive at a pivotal time.

The Electricity Services Entry Mechanism (ESEM) is the Nelson Review’s flagship reform and offers a sophisticated solution to the “tenor gap” problem that has plagued project financing.

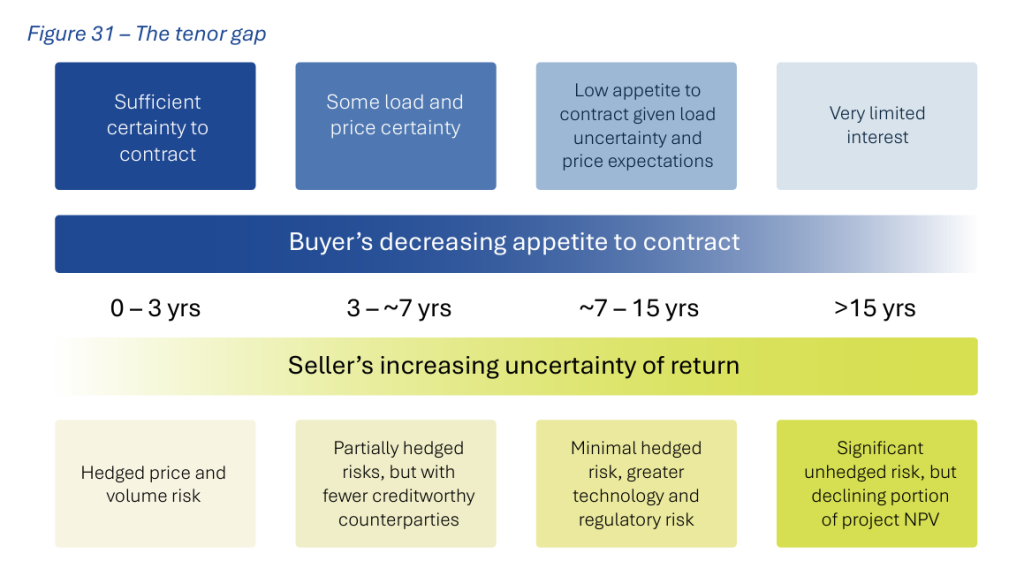

Tenor gap problem

The Nelson Review identifies a fundamental mismatch between project financing needs and market appetite for long-term contracts. Capital intensive renewable and storage projects often require revenue certainty over 15+ years to secure financing. However, retailers and commercial and industrial (C&I) energy users typically contract for only 1-7 years.

This “tenor gap” creates a critical contracting void in later project years, resulting in a bankability challenge without government support. The review’s ESEM solution centres on bridging this gap through standardised, tradeable contracts.

How the ESEM works

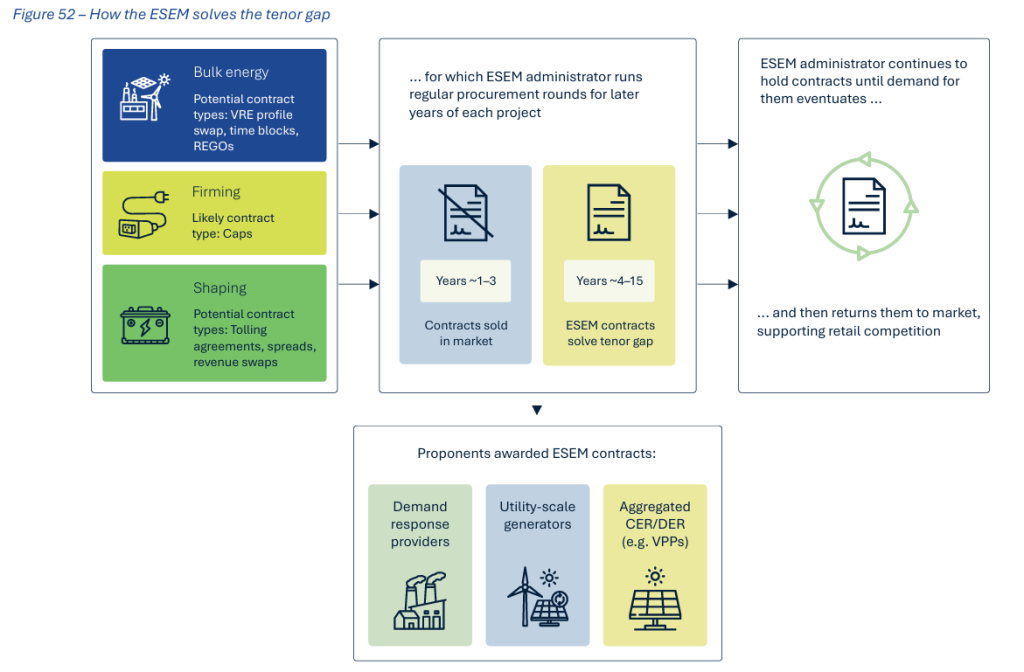

The ESEM is intended to replace the CIS and be a permanent contracting framework embedded in National Electricity Law. It addresses the tenor gap through an innovative “warehouse and recycle” model that provides long-term revenue certainty while maintaining market mechanisms.

Like the CIS, the ESEM will be a voluntary mechanism. Developers will be free to continue with new investments outside of the ESEM, if they wish.

Three ESEM services

The ESEM Administrator will conduct competitive reverse auctions to procure standardised, fungible financial derivative contracts from new projects for three specific services:

- Bulk zero-emissions energy

- Shaping services

- Firming services

“Shaping” and “firming” services sound very similar, but the final report makes a distinction in requiring firming services to be “capable of being dispatched continuously for the time it takes to reach the Cumulative Price Threshold if prices are at the Market Price Cap”. If we use FY 2025-26 as an example, where the CPT is set to $1,823,600/MWh and MPC is $20,300/MWh, this implies a duration requirement of 7.5 hours.

Projects will be able to bid for multiple services if their capabilities allow. For example, pumped hydro could offer both shaping and firming services.

The ESEM is expected to be open to all providers of a given service, including CER aggregators and demand response providers, provided these resources will be scheduled for dispatch by AEMO. The final report also suggests that gas could be eligible, in contrast to the CIS.

The ESEM Administrator would be required to procure resources consistent with state and territory electricity sector emissions targets.

Move to standardised contracts

ESEM contracts will be based on standardised structures developed through an industry-led co-design process.

The review highlights emerging contract forms such as VRE profile swaps (which better match renewable generation patterns) and virtual tolling agreements for batteries. These contracts are currently traded over-the-counter but not available on the ASX. The intent is to make these contracts more standardised and fungible than current bespoke arrangements, with the aim of eventually being traded on an exchange platform. For this to occur, the contracts would need to be financial in nature (i.e. not tied to physical plant operations). That being said, the contracts would be contingent on plant commissioning to ensure a successful bid results in the new project being built.

Furthermore, ESEM contracts will be designed to allow developers to recover all their efficient costs, not just the minimum revenue to attract financing as is the case for the CIS.

The final report has also recommended smaller parcels to reflect the smaller nature of individual generators (e.g. 100 kW rather than 1 MW).

ESEM contracts start three years in

The critical innovation is that ESEM only contracts the “later years” of a project’s operational life, specifically the period after projects have secured their own commercial contracts in-market.

The final report reduced the required in-market period from the draft’s 5-7 years to a flexible minimum of 3 years. This was a direct response to industry feedback that seven years was prohibitively long.

The ESEM Administrator has discretion to adjust this based on market conditions and technology maturity. For example, the Administrator could run special tenders supporting technology-specific targets such as offshore wind or pumped hydro, with calibrated in-market periods recognising their unique development barriers and longer lead times.

Warehouse and recycling process

Once the ESEM Administrator purchases these long-dated contracts from developers through competitive auctions, it acts as a central warehousing entity, holding contracts until natural demand materialises from retailers and C&I users.

The Administrator then progressively sells these contracts back into the forward market, recycling them at prices reflecting actual market conditions. This progressive recycling serves multiple purposes:

- Provides bankable revenue certainty to support project finance;

- Maintains forward market liquidity by ensuring contracts are available when buyers need them;

- Supports retail competition by enabling retailers to offer longer-term price certainty to customers; and

- Improves price transparency in long-dated derivative markets.

The mechanism effectively takes a long position on future electricity services on behalf of consumers. It then offloads that position gradually as the market absorbs it over time. For a battery project, this means securing a 10-15 year revenue stream for shaping and/or firming services while operating commercially for the first 3+ years.

ESEM implementation timeline

The Panel has urged energy ministers to implement the ESEM as soon as possible. This would involve piloting the ESEM by end of 2026, followed by a formal start in early 2027 to minimise the gap following the conclusion of the CIS.

All NEM states except Queensland have provided in-principle agreement to the Nelson Review’s core recommendations. Queensland acknowledged the panel’s work while maintaining jurisdictional sovereignty over implementation, leaving open how it will address similar challenges within its market framework.

For utility-scale renewable and storage developers, the path forward requires preparation for greater market integration, embracing standardised contracting frameworks, and positioning projects to access ESEM support for the critical later-year revenue gap.

The reforms won’t eliminate all development challenges. Grid connection, planning approvals, and construction risks remain, but the ESEM establishes a predictable pathway for financing firmed renewable generation and storage at the scale Australia’s energy transition demands.

With most ministerial support secured and implementation underway, developers should engage actively in the co-design processes throughout 2026 to ensure contracts and frameworks serve project needs while advancing system-wide objectives.

Energy Synapse specialises in market modelling, revenue modelling, and strategic advisory for utility-scale renewable energy and storage projects. Learn more about how we can help.