The debate about the need for baseload coal-fired power stations has reignited this week. Energy Minister Josh Frydenberg was quoted as saying he “would welcome a new coal-fired power station for our country because it supplies reliable baseload power and it has served us well in the past and will continue to serve us well in the future”.

There is no doubt that coal has played a significant role in the National Electricity Market (NEM). But can it provide any value in a future highly renewable grid?

Baseload power is a business model, not a technical requirement

Baseload generators such as coal-fired power stations (or nuclear in other markets) have very high fixed costs, but low marginal costs, and are relatively slow at starting up and ramping up and down. In contrast, natural gas generators have low fixed costs, but high marginal costs and are much quicker to start and ramp.

It is from these characteristics that the concept of baseload and peaking generation emerges. The most economic mode of operation for a coal-fired power station is to run at a steady, constant level more or less 24/7. In contrast, the economic characteristics of gas mean that it is better suited to meet the more variable and dynamic portion of electricity demand.

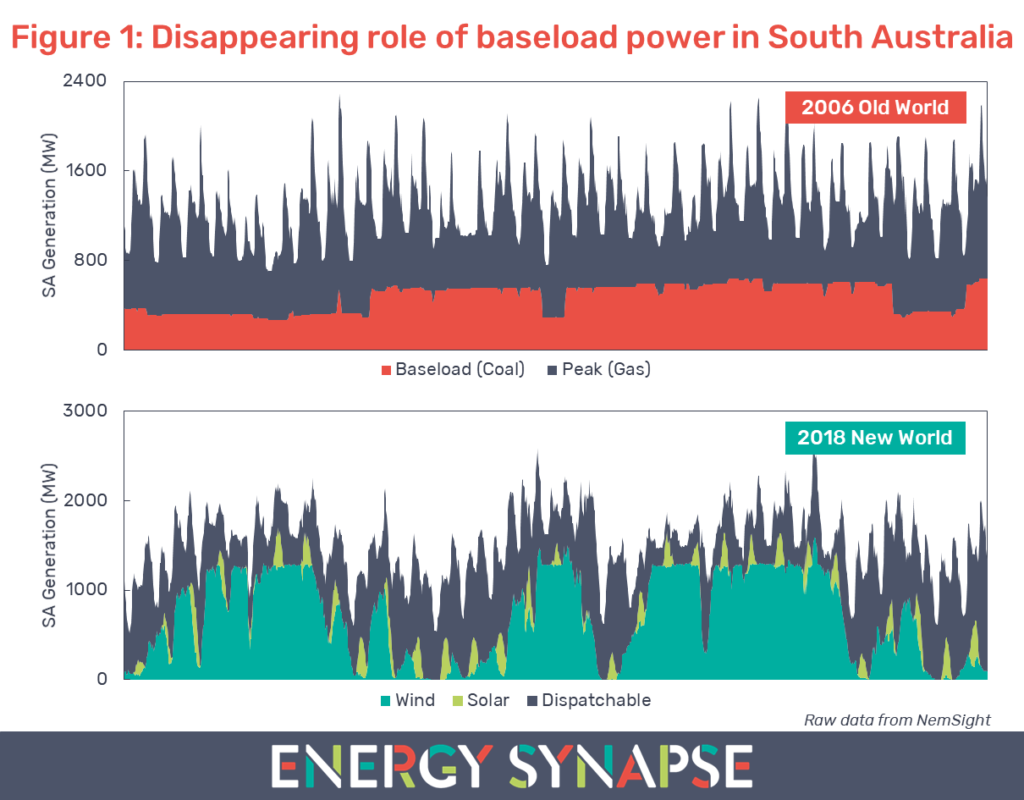

No role for baseload coal in South Australia

Figure 1 shows electricity generation in South Australia for the previous month (23 May to 22 June 2018) compared with the same period in 2006. We compiled this data using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Back in 2006, there was virtually no renewable energy in South Australia aside from a tiny amount of rooftop solar (<2 MW). The generation mix consisted of brown coal and natural gas. As can be seen from Figure 1, these generators followed the old world paradigm of baseload and peaking generation.

This is in stark contrast to the new world in 2018. For the 31 day period in question, just over 50% of the energy generated in South Australia came from variable renewable energy (wind power, rooftop solar, and large scale solar). The remaining generation came from dispatchable sources, consisting primarily of gas along with a smaller amount of battery storage and diesel generation. There has been no coal in South Australia since the closure of Northern Power Station in May 2016.

As can be seen from Figure 1, in a highly renewable grid, there is no steady profile left for baseload power to service. A power station that runs at a constant level provides no value or enhancement to reliability in this type of system. What is needed is highly flexible and fast responding power. This can come from a variety of sources such as gas, hydro, energy storage, and demand response. However, coal is not one of them.

Renewable energy not to blame for high electricity prices in South Australia

Some people reading this may look at Figure 1 and immediately conclude that the replacement of coal with renewables has lead to high power prices in South Australia. However, South Australia has always had high prices relative to the rest of the NEM. Data from AEMO shows that in 16 out of the last 20 financial years, South Australia either had the highest or second highest wholesale electricity price. This comes about from South Australia having a peaky demand profile, being over reliant on gas, and a lack of competition in the market, among other factors.

Electricity demand must be in balance with supply at every point in time. This is a true technical requirement. However, there are a number of ways to meet this requirement. The economic characteristics of coal and gas led to the baseload/peaker paradigm. In the new world, flexibility is king and this means that the economics of coal are just not going to stack up.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter

Four months in, SA Tesla battery is showing mixed results in energy arbitrage

April 5, 2018

Share

Tesla’s big battery in South Australia was officially switched on in late November 2017. At 100 MW/129 MWh, it is the largest lithium ion battery in the world and signals the beginning of a new era in how we manage the electricity system. In this article, we take a look at how the battery has operated in its first four months.

Before we delve any further, it is important to note that the Tesla battery is really two systems:

70 MW/10 MWh is contracted to the South Australian state government for the purpose of providing grid stability services;

The remaining 30 MW/119 MWh can be used by the Hornsdale operator to trade in and arbitrage the energy market.

The economic viability of large scale batteries is largely dependent on how much revenue they are able to extract from the wholesale energy market and the various ancillary service markets. In this article, we will focus on the economic performance of the battery in the energy market only.

We use a software called NemSight by Creative Analytics (part of the Energy One group) to analyse the operation and bidding behaviour of the Tesla battery.

Tesla battery is being heavily utilised

The Tesla battery is certainly not sitting idle in the market. Figure 1 shows the operation of the Tesla battery on a five minute basis from 1 Dec 2017 to 31 Mar 2018. As can be seen, the battery is being utilised very frequently. In fact, in 63% of the dispatch intervals, the battery was either being charged or discharged. Only 37% of the time was the battery not being used in any way. Furthermore, nearly 40% of these zero utilisation periods occurred in December while the battery was still being tested.

From Dec 2017 to Mar 2018, the Tesla battery consumed an average of 116 MWh per day for charging. In contrast, it delivered an average of 94 MWh per day back into the grid. From this we can work out that the average efficiency of the battery has been 82%. As expected, the efficiency of the battery is lower under real world conditions than the spec sheet efficiency of 88%, which is calculated at 25°C.

Tesla battery made $1.4 million in the energy market, but is losing money 47% of the time

Figure 2 shows our estimate of the value that the Tesla battery received from selling electricity into the energy market versus the cost of buying electricity to charge the battery. We estimate the total net revenue from the energy market to be just under $1.4 million. The overwhelming majority of this came in January 2018 when the energy market experienced the highest volatility. In contrast, the Tesla battery barely made any money in December and March.

When arbitraging the spot market, the aim of the game is the same as trading stocks: buy low, sell high. A crucial difference is that you not only have to sell at a price which is higher than your buy price, but you also have to cover the cost of the extra energy that is needed to charge the battery (because energy efficiency is less than 100%). Therefore, the days with the most volatile pricing offer the biggest opportunities for arbitrage. Figure 3 shows that the Tesla battery made 95% of its net revenue in just five (very volatile) days.

If we exclude these five days, the average net revenue for the battery is a measly $530 per day. In fact, on 57 days (47%) the Tesla battery actually lost money in the energy market. The total losses over the 57 days add up to about $135,000. As mentioned earlier, this analysis looks at the revenue from the energy market only. It does not include any of the revenue received from providing ancillary services. Nonetheless, our numbers do suggest that the operators of the battery will need to be careful to avoid needlessly cycling the battery for little financial gain. This is an important consideration because the lifetime of a battery is strongly related to how many times it is cycled.

Furthermore, “buy low, sell high” is not as easy as it sounds. The energy market is incredibly complex. In our experience, a successful bidding strategy needs to be underpinned by advanced predictive analytics and co-optimisation. Failure to do so can result in the asset significantly undershooting revenue expectations. Some food for thought as the race to build big batteries begins.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter