National Electricity Market year in review part 2/2: Changing energy mix

January 18, 2019

In the second installment of our National Electricity Market (NEM) Year in Review series, we will be looking at how the energy mix has evolved ov ...

January 18, 2019

In the second installment of our National Electricity Market (NEM) Year in Review series, we will be looking at how the energy mix has evolved ov ...

January 8, 2019

2018 has been another challenging year for the energy industry. Hopes of a national policy that merges energy and emissions were dashed with the ...

November 25, 2018

Wind farms in South Australia contributed 42% to electricity generation within the state in the first 22 days of November. Gas generation also co ...

October 31, 2018

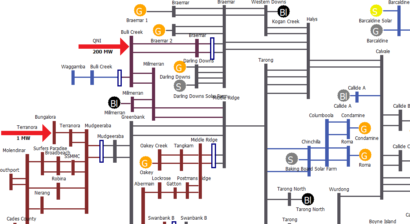

2018 is already a record year for solar PV in Australia, and in particular, the utility scale sector. Queensland (QLD) leads the nation across se ...

June 27, 2018

The debate about the need for baseload coal-fired power stations has reignited this week. Energy Minister Josh Frydenberg was Read more >

May 30, 2018

From 1 July 2021, the National Electricity Market (NEM) in Australia will be settled Read more >

February 27, 2018

Midway through February 2018, Queenslanders sweltered through a severe heatwave, which saw statewide average temperatures exceed 40°C for severa ...

February 1, 2018

Victoria has traditionally been considered the “boring state” when it comes to volatility in wholesale electricity prices. But that all chang ...