Batteries in South Australia earn $1 million over two days

December 24, 2019

Share

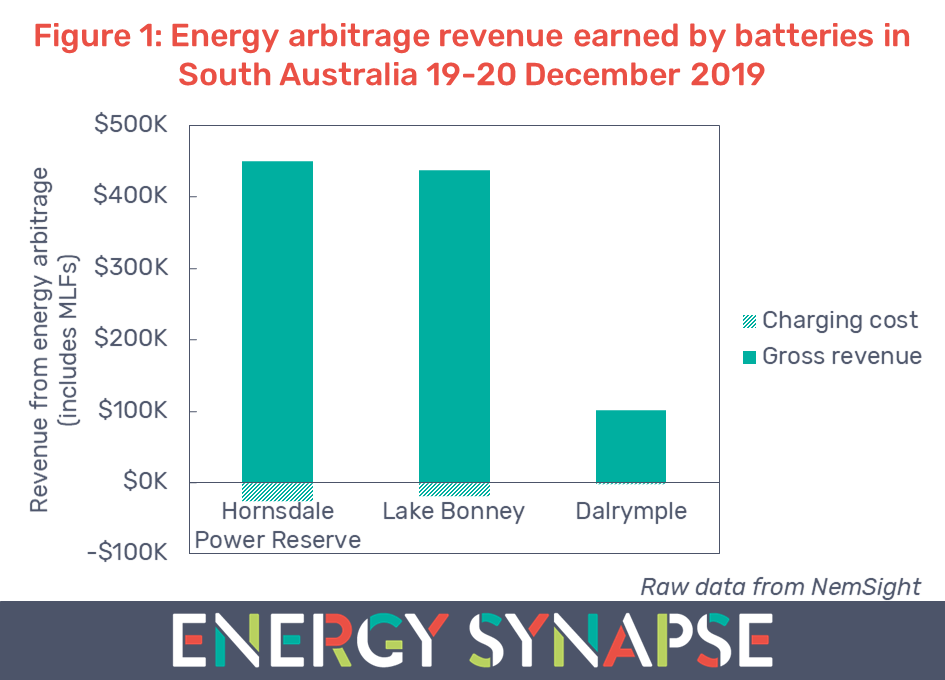

Grid-scale batteries in South Australia earned almost $1 million from the energy market over two days from 19-20 December 2019 (see Figure 1) as the nation sweat through an extreme heatwave.

This revenue is just from arbitraging the wholesale energy market and includes the cost of charging the batteries as well as marginal loss factors (MLFs). It does not include revenue from frequency control ancillary services (FCAS) or any bilateral contracts.

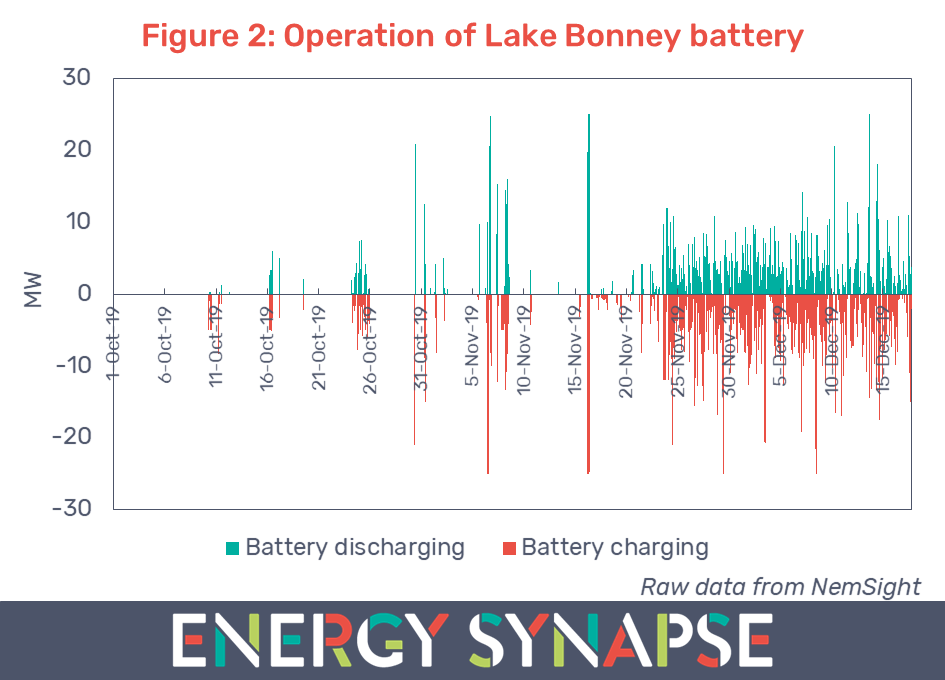

These earnings will be especially welcome news for Infigen’s new 25 MW/52 MWh Lake Bonney battery. The Lake Bonney battery, which cost $38 million, was only recently energised (October 2019) and appears to have started commercial operation in late November (see Figure 2).

The 100/129 MWh Hornsdale Power Reserve (HPR) has been operating the longest (since late 2017). Despite being a bigger battery, the HPR earned similar revenue to the Lake Bonney battery. This is because the HPR has only 30 MW/119 MWh available for commercial operation in the energy market.

We recently published a comprehensive 21 month analysis of how the Hornsdale battery has been operating, bidding, and earning revenue from energy arbitrage and all eight FCAS markets. Our independent analysis is supported by the Australian Energy Storage Alliance and has proven to be a very valuable resource for developers and investors of battery storage. In 2020, the HPR will be getting 50% bigger and will be demonstrating a range of new grid services, including fast frequency response.

Batteries seize opportunity as Australia sweats through three hottest days on record

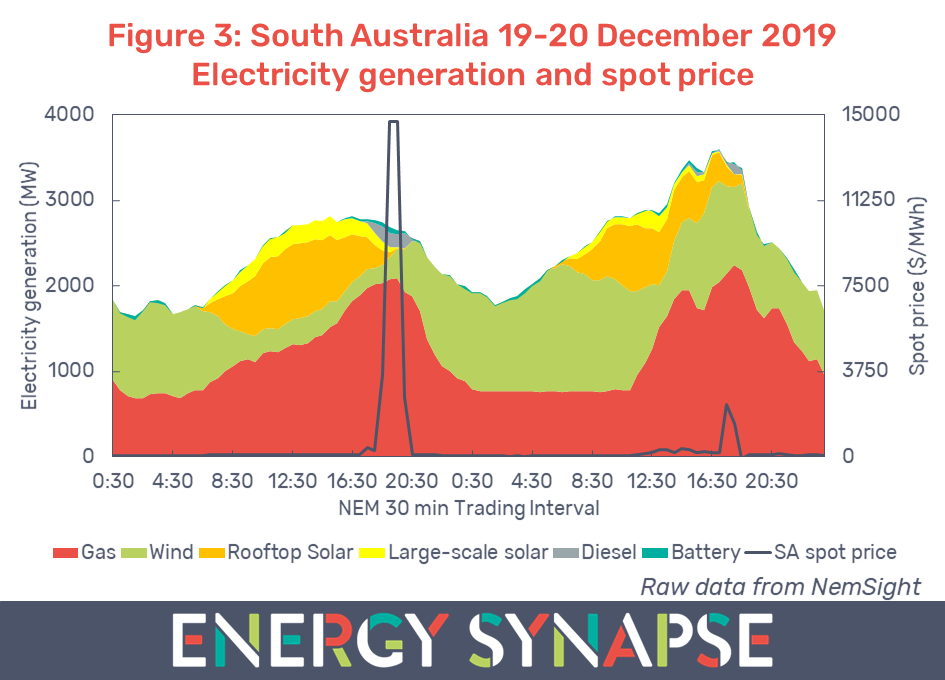

The very high daily revenue earned by batteries last week coincided with the first price volatility of the season. The spot price in South Australia hit the market cap of $14,700/MWh for an hour on Thursday 19 December (see Figure 3). Tuesday, Wednesday, and Thursday of that week were the three hottest days ever recorded in Australia.

Figure 3 shows that the high pricing also coincided with low electricity generation from wind and solar. As a result, expensive gas and diesel generators were needed to meet demand. Being both dispatchable and fast responding, batteries were well placed to take advantage of this volatility in pricing.

This highlights a broader economic challenge for wind and solar farms. Wind and solar farms have a marginal cost of zero. As a result, they put significant downward pressure on electricity prices at the time at which they are generating electricity. However, because they are weather dependent, their operators cannot ramp up production to take advantage of high prices.

As the uptake of variable renewable energy grows, the earnings gap between renewables and other market participants will continue to increase. Energy storage is of course, one of the solutions to this problem. Thus, we can expect renewable energy projects to increasingly incorporate storage to help manage this risk.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter

Wholesale electricity prices reach record highs

August 29, 2019

Share

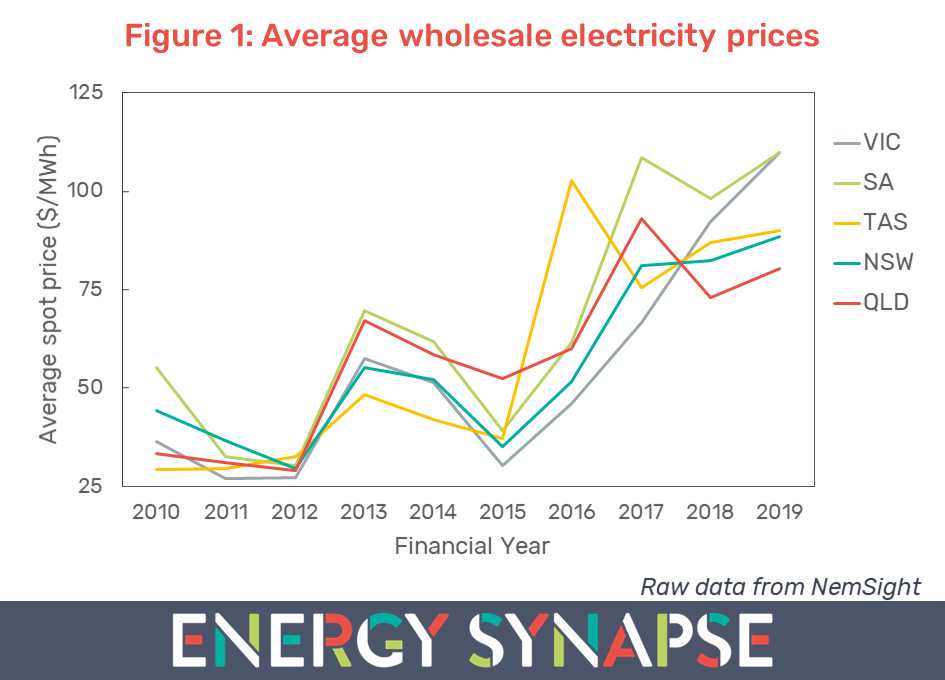

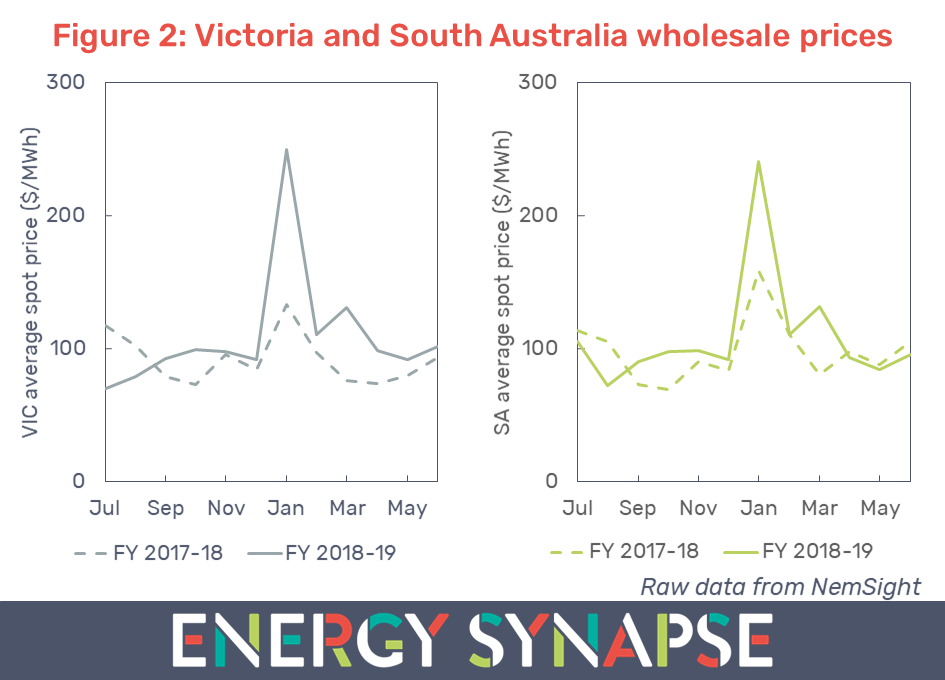

Financial year ending June 2019 saw wholesale electricity prices rise in every state in the National Electricity Market (NEM). Victoria had the highest increase on the previous financial year at 19%, followed by South Australia (12%), Queensland (10%), New South Wales (8%), and Tasmania (3%) (see Figure 1). This data has been compiled using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Wholesale electricity prices have tripled over the past decade in Victoria and Tasmania and have doubled in Queensland, NSW, and South Australia. This energy crisis has been brought about by a combination of factors coming together. These include high gas prices, a decade of policy uncertainty, exit of ageing generation, lack of competition, outdated market rules, and more. And it is still very much on-going. Prices in South Australia, Victoria, and NSW all reached record highs in the 2019 financial year.

Pricing in Tasmania peaked earlier in FY 2016, due to a prolonged outage of the Basslink interconnector, which links to the mainland grid.

Queensland peaked in FY 2017. In mid 2017, the Queensland Government directed state owned generators to alter their bidding practices and put downward pressure on wholesale electricity prices. This direction has been one of the main reasons why Queensland has had the lowest wholesale electricity prices in the NEM for the last two years, despite growing max demand. However, this bidding direction ended on 30 June 2019. It will be interesting to see whether the bidding behaviour from state owned generators reverts back to old patterns over the coming summer.

Victoria and South Australia battled record heat and coal failures

High summer prices drove the annual price increase in Victoria and South Australia as seen in Figure 2. This was largely weather related as Australia sweltered through the hottest summer on record.

However, it was also due to multiple failures at Victorian coal-fired power stations, particularly on the 24th and 25th of January. An extreme heatwave gripped South Australia and Victoria, with some regions experiencing record high temperatures. Multiple brown coal outages led to 1.1 GW of thermal generation being unavailable on 24 January and 1.6 GW being unavailable on 25 January (see report by AEMO). This created a shortage of supply, with the unfortunate result of load shedding in Victoria and record high electricity prices.

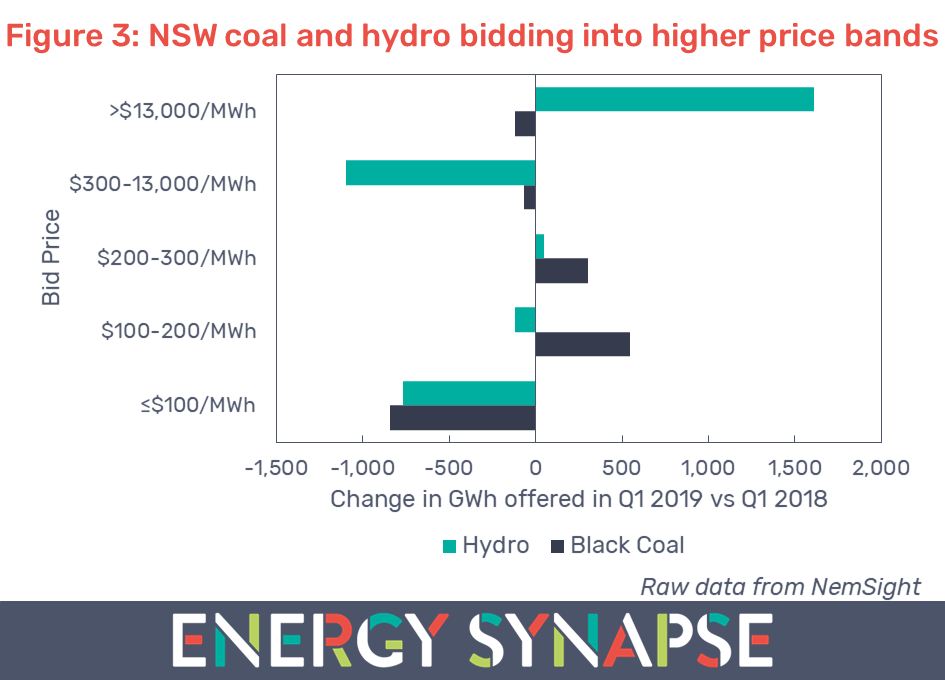

NSW coal and hydro generators raised bids

In contrast to Victoria and South Australia, pricing in NSW was not particularly volatile. The main contributing factor to higher prices was a change in bidding behaviour from coal and hydro generators during the first quarter (Jan to Mar) of 2019.

Figure 3 shows that black coal generators reduced the amount of electricity they offered in price bands ≤$100/MWh and instead bid this energy into higher price bands between $100/MWh and $300/MWh.

The change in bidding behaviour was even more drastic for hydro generators, who significantly cut bids in the ≤$100/MWh and $300-13,000/MWh price bands and instead bid this energy at prices greater than $13,000/MWh. Dry conditions and low storage levels were contributing factors.

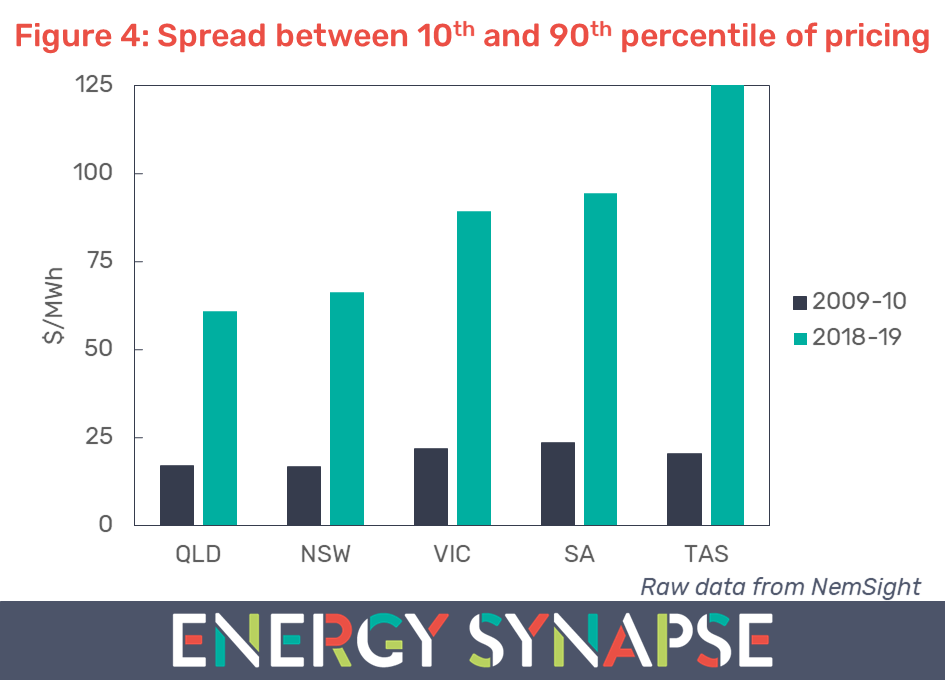

Spreads in wholesale electricity prices on the rise

Another interesting trend over the past decade has been the growing spread (or difference) between the 10th and 90th percentile of pricing. This has interesting implications for energy storage, which is most economic when spreads are high.

Figure 4 shows the spread for each region in the NEM in the last financial year versus 10 years prior. Ten years ago, spreads very were small, varying between $17-24/MWh across states. This offered limited arbitrage opportunities in the spot market. In contrast, in the last financial year, spreads ranged from $60/MWh to $125/MWh. As an example, the Tesla big battery in South Australia achieved an average price differential of $76/MWh (inclusive of round trip efficiency losses).

As more zero marginal cost renewable energy enters the market, we can expect wholesale prices to keep decreasing at the times when renewables are generating power.

Queensland gave the perfect example earlier this week when daytime prices hit zero/negative for a record nine consecutive days. This was predominantly due to high solar uptake, low electricity demand, and inflexible coal. RenewEconomy covered some of our commentary here and here.

In contrast, when renewable energy is less available, prices tend to go up. The opening up of spreads is a predictable outcome of the transition to renewable energy. It will be largely up to energy storage, as well as demand response, to regulate spreads going forward.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter