Hornsdale Power Reserve earns record revenue in September 2019

October 21, 2019

Share

The world’s biggest lithium-ion battery, the 100 MW/129 MWh Hornsdale Power Reserve in South Australia, has just earned its biggest monthly revenue from wholesale markets.

The ‘Tesla big battery’ as it is commonly known, was famously brokered via a deal on Twitter and has been operating in Australia’s National Electricity Market (NEM) since late 2017. We recently published independent analysis, which provides a deep dive into the operation, merchant revenue, and bidding strategies of the Hornsdale Power Reserve from January 2018 to September 2019. In this article, we look at just one of the many insights from the report.

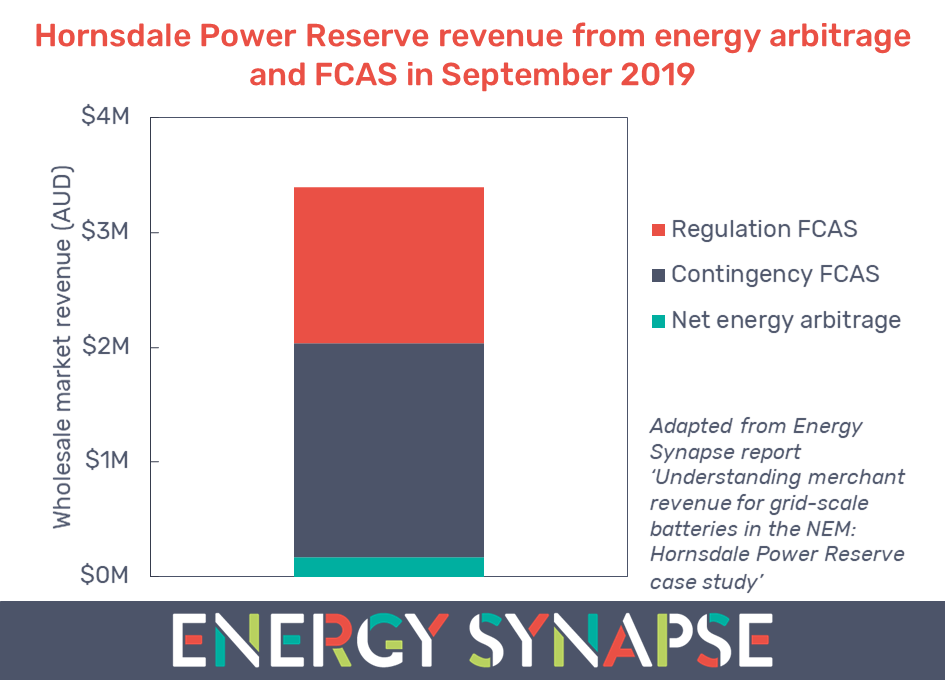

Our analysis shows that the Hornsdale battery earned approximately $3.4 million from wholesale markets in September 2019 (see chart below). This is the highest monthly revenue that the battery has achieved. Note that this is inclusive of the cost of charging the battery. However, it does not include non-market revenue streams (such as the contract it has with the South Australian government), FCAS payments under the causer pays methodology, or any other factors which are private to the operator.

The overwhelming majority of revenue in September came from providing frequency control ancillary services (FCAS). Contingency services, which correct major frequency deviations in the grid, accounted for the highest share of revenue (55%). This was due to a strong rebound in contingency FCAS prices. In September 2019, the Australian Energy Market Operator (AEMO) made changes to how it calculates FCAS requirements. This has resulted in a higher volume of contingency FCAS being procured, which has contributed to the upward pressure on prices.

Operating batteries has a learning curve

At a high level, the revenue that a battery can earn each month and how this is split across various markets, depends on two factors:

1. Prevailing market conditions; and

2. The strength of the battery’s trading strategy.

The Hornsdale battery may have earned the single highest monthly revenue in September, but it also missed significant opportunities throughout the month. In our analysis, we compare the actual operation of the Hornsdale Power Reserve with our optimised operation model. This comparison shows that there was potentially more than $1.1 million of additional revenue available in the market in September. This highlights the complexities of operating batteries under real world conditions and uncertainties.

Batteries are unlike any other asset in the NEM. A generator, such as a coal or gas plant, can theoretically keep producing electricity as long as the fuel continues to be supplied. In contrast, a battery has a limited capacity to charge or discharge energy at any point in time. As a result, previous charge/discharge decisions can have a big impact on future revenue. There is still much to learn about how to operate batteries in the most profitable way.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter

Gas generators getting 20% higher price than wind farms in South Australia

November 25, 2018

Share

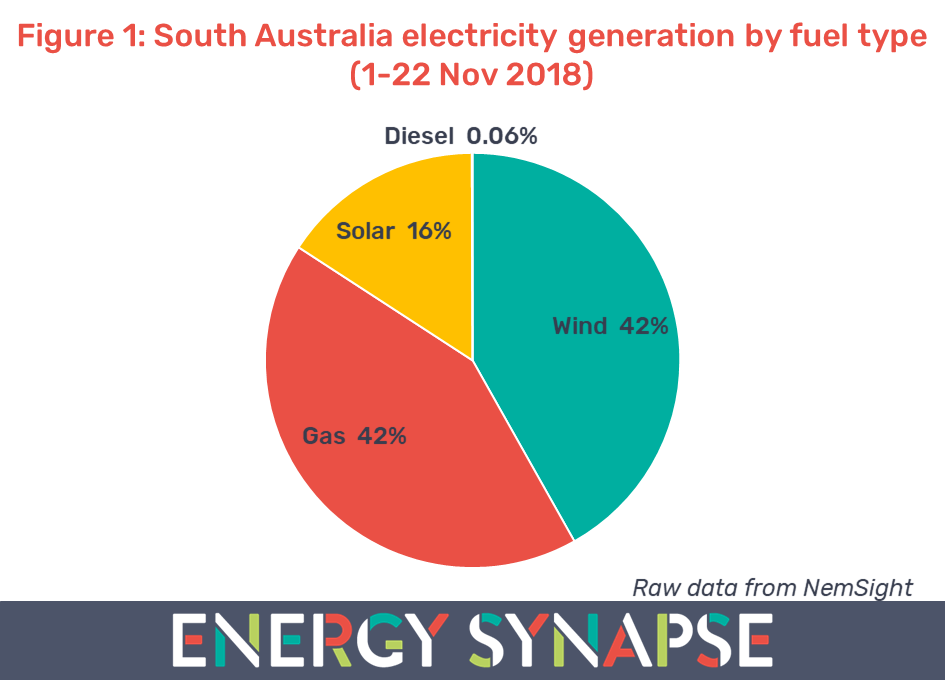

Wind farms in South Australia contributed 42% to electricity generation within the state in the first 22 days of November. Gas generation also contributed 42% as seen in Figure 1. Solar came in third at 16%. The vast majority of this (84%) came from rooftop solar PV. We have compiled this data using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Despite the fact that gas generators and wind farms generated almost identical amounts of electricity, they received very different prices for their power. On aggregate, wind farms received an average price of $87/MWh from the spot market. In contrast, gas generators received a price $18/MWh (20%) higher. Note that we have not adjusted these figures for marginal loss factors (MLFs) in order to isolate the effect of price alone.

Solar and wind farms pushing down wholesale electricity prices

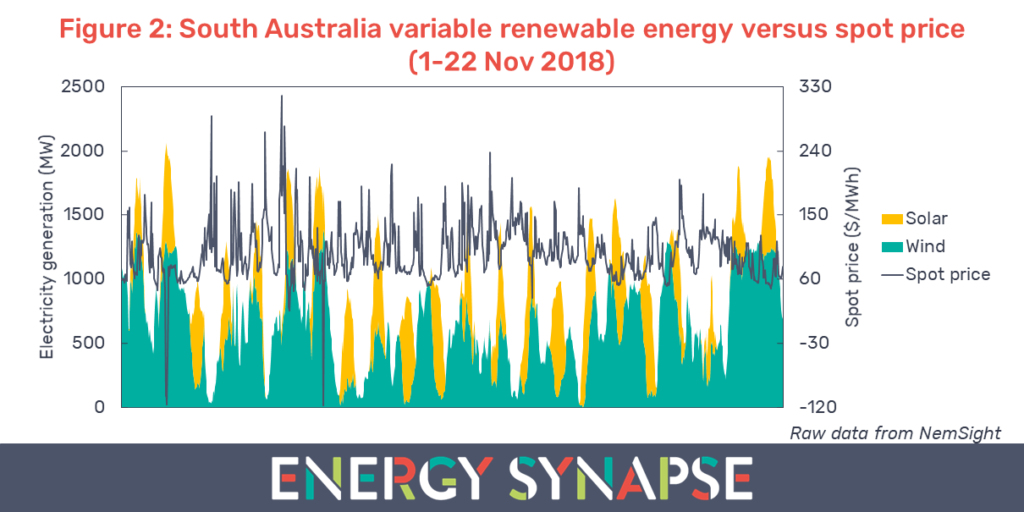

Figure 2 shows the electricity generation from wind farms and solar (both rooftop and large scale). Overlaid on top of this is the 30 minute spot price. We can see that when total generation from variable renewables is low, the price tends to be higher. In contrast, when variable renewables are generating high amounts of power, the price dips.

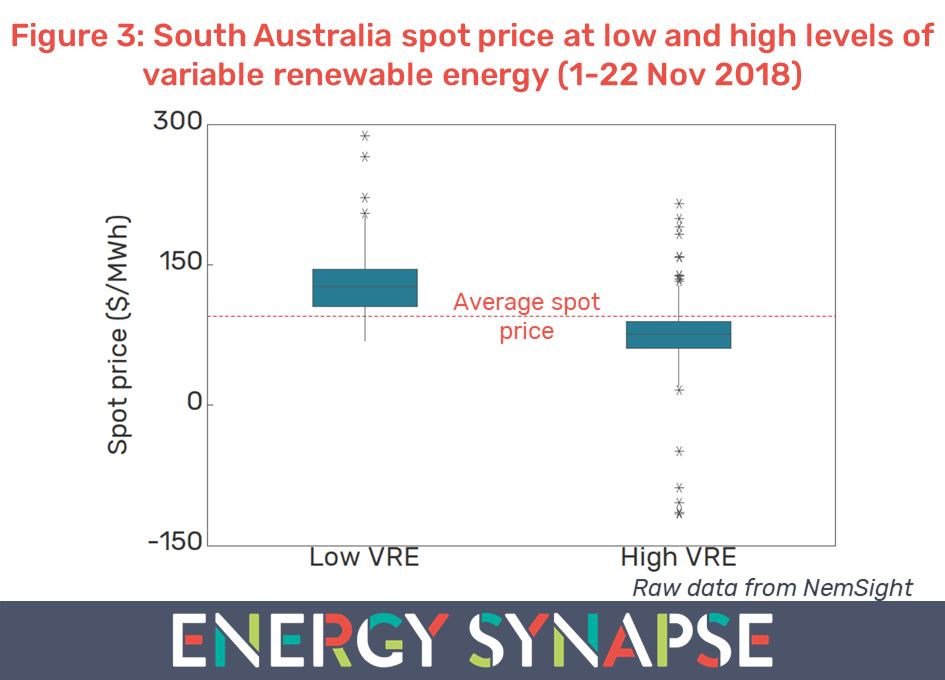

Figure 3 shows this effect more clearly. Here we see the distribution of spot prices in two scenarios: low variable renewable energy (≤ 250 MW) and high variable renewable energy (≥ 1000 MW). We have also shown the average spot price as a red dotted line. Figure 3 shows that wholesale electricity prices are significantly lower when output from variable renewables is high.

Price setting in the NEM

In the National Electricity Market (NEM), generators submit bids to AEMO for each five minute dispatch interval. They state how much electricity they are willing to supply and at what price. These bids are then ordered from least to most expensive. The least cost generators (taking into account constraints) are dispatched to serve the demand in the market. The marginal bid (i.e. the last/highest cost generator that is selected) sets the price for everyone in that dispatch interval.

Rooftop solar is already subtracted from demand before we even get to this selection process. Large scale solar and wind farms have a zero marginal cost and hence tend to bid into the market at or below $0/MWh. Therefore, when wind and solar are generating a lot of power, we have high amounts of zero price generation in the market. This means that the market clears at a lower price. In contrast, when there is low generation from wind and solar, the market is more reliant on more expensive generation sources (e.g. gas) and hence clears at a higher price.

Flexibility will become increasingly valuable

Wind and solar have the advantages of being clean, renewable and cheap. However, their major disadvantage is that they are weather dependent and hence difficult to control.

As more and more wind and solar generation enters the market, the wholesale price of electricity will become lower and lower at the times when generation output is high from these assets. In contrast, power sources that are flexible and controllable (e.g. gas, hydro, batteries, demand response etc) and able to ‘fill in the gaps’ in Figure 2, will become increasingly valuable.

Another implication of this is that variable renewables may not be able to provide an effective hedge against prices spikes in the wholesale market. Therefore, any retailers or large energy users who are considering adding high levels of renewables to their portfolios, will also need to think about how to complement this with dispatchable power sources.

Want to know more about how solar and wind farms are performing in the NEM and what revenues they are receiving? Get a copy of our detailed analysis.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter