Gas generators getting 20% higher price than wind farms in South Australia

November 25, 2018

Share

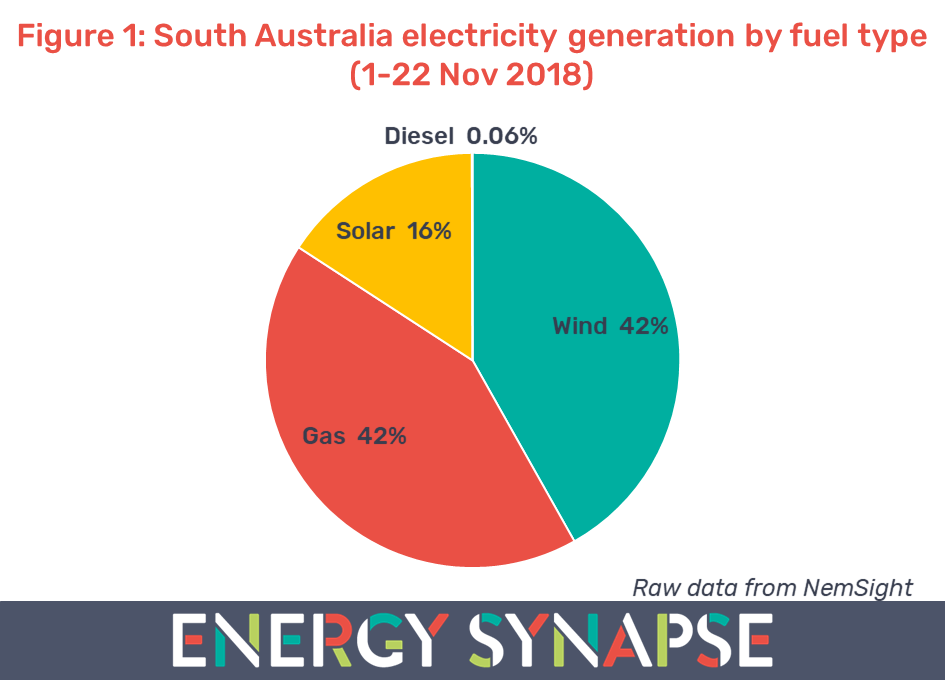

Wind farms in South Australia contributed 42% to electricity generation within the state in the first 22 days of November. Gas generation also contributed 42% as seen in Figure 1. Solar came in third at 16%. The vast majority of this (84%) came from rooftop solar PV. We have compiled this data using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Despite the fact that gas generators and wind farms generated almost identical amounts of electricity, they received very different prices for their power. On aggregate, wind farms received an average price of $87/MWh from the spot market. In contrast, gas generators received a price $18/MWh (20%) higher. Note that we have not adjusted these figures for marginal loss factors (MLFs) in order to isolate the effect of price alone.

Solar and wind farms pushing down wholesale electricity prices

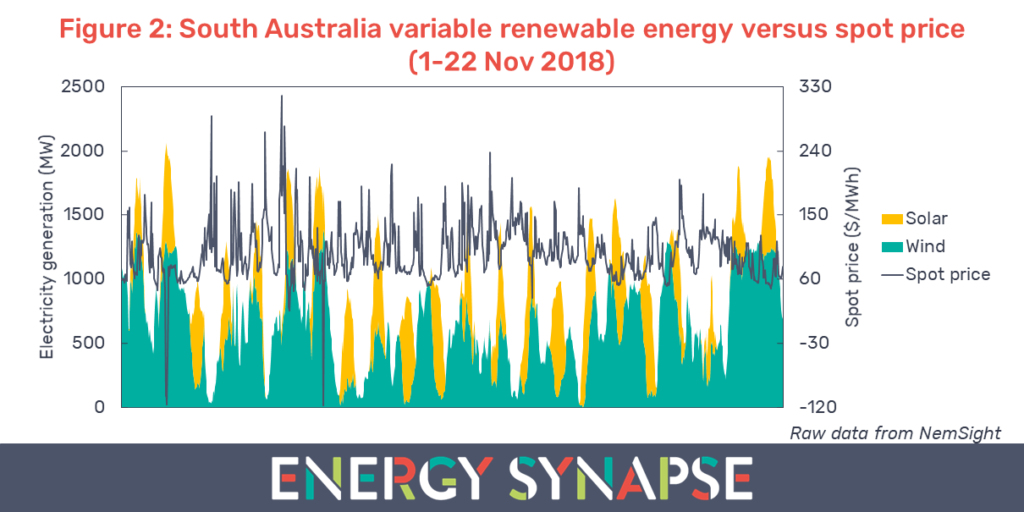

Figure 2 shows the electricity generation from wind farms and solar (both rooftop and large scale). Overlaid on top of this is the 30 minute spot price. We can see that when total generation from variable renewables is low, the price tends to be higher. In contrast, when variable renewables are generating high amounts of power, the price dips.

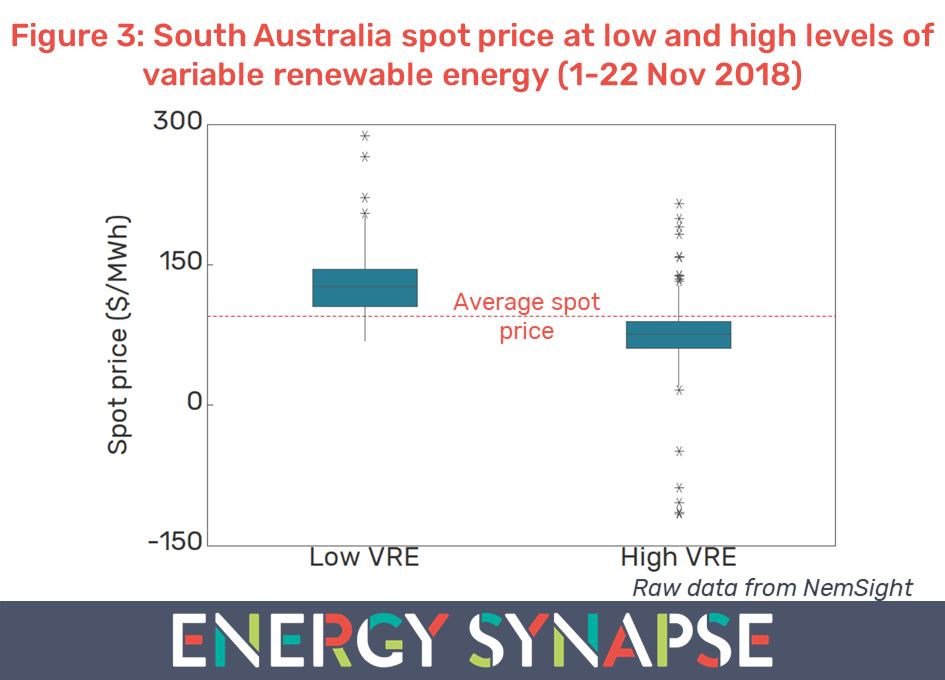

Figure 3 shows this effect more clearly. Here we see the distribution of spot prices in two scenarios: low variable renewable energy (≤ 250 MW) and high variable renewable energy (≥ 1000 MW). We have also shown the average spot price as a red dotted line. Figure 3 shows that wholesale electricity prices are significantly lower when output from variable renewables is high.

Price setting in the NEM

In the National Electricity Market (NEM), generators submit bids to AEMO for each five minute dispatch interval. They state how much electricity they are willing to supply and at what price. These bids are then ordered from least to most expensive. The least cost generators (taking into account constraints) are dispatched to serve the demand in the market. The marginal bid (i.e. the last/highest cost generator that is selected) sets the price for everyone in that dispatch interval.

Rooftop solar is already subtracted from demand before we even get to this selection process. Large scale solar and wind farms have a zero marginal cost and hence tend to bid into the market at or below $0/MWh. Therefore, when wind and solar are generating a lot of power, we have high amounts of zero price generation in the market. This means that the market clears at a lower price. In contrast, when there is low generation from wind and solar, the market is more reliant on more expensive generation sources (e.g. gas) and hence clears at a higher price.

Flexibility will become increasingly valuable

Wind and solar have the advantages of being clean, renewable and cheap. However, their major disadvantage is that they are weather dependent and hence difficult to control.

As more and more wind and solar generation enters the market, the wholesale price of electricity will become lower and lower at the times when generation output is high from these assets. In contrast, power sources that are flexible and controllable (e.g. gas, hydro, batteries, demand response etc) and able to ‘fill in the gaps’ in Figure 2, will become increasingly valuable.

Another implication of this is that variable renewables may not be able to provide an effective hedge against prices spikes in the wholesale market. Therefore, any retailers or large energy users who are considering adding high levels of renewables to their portfolios, will also need to think about how to complement this with dispatchable power sources.

Want to know more about how solar and wind farms are performing in the NEM and what revenues they are receiving? Get a copy of our detailed analysis.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter

QLD solar is booming and pushing down daytime electricity prices

October 31, 2018

Share

2018 is already a record year for solar PV in Australia, and in particular, the utility scale sector. Queensland (QLD) leads the nation across several metrics as shown by the latest data from the Australian PV Institute (APVI) released on 25 October 2018:

(i) QLD has the highest total installed capacity (3,536 MW) out of any state;

(ii) QLD has the highest residential rooftop solar penetration by both capacity (1,935 MW) and percentage of dwellings (32.6%); and

(iii) QLD has the highest large scale (100+ kW) solar PV capacity (1,316 MW).

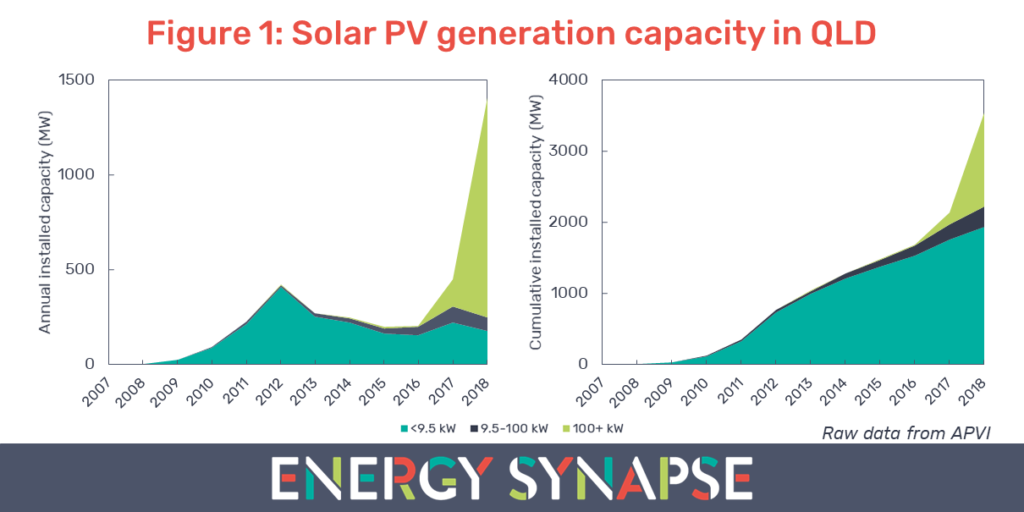

Figure 1 shows the annual and cumulative generation capacity for solar PV in QLD from 2007 to present. The data is segmented by system size: <9.5 kW (residential), 9.5-100 kW (small commercial & industrial), and 100+ kW (large C&I and utility generation).

More solar has been added to the QLD grid in the first 10 months of 2018 than in the previous five years combined. 2018 is also the first year where the deployment of large scale solar (100+ kW) has exceeded small scale solar. 88% of the large scale solar generation capacity in QLD comes from solar farms 50+ MW in size. This extraordinary growth in utility scale systems has come about from a combination of drastic decreases in the cost of solar as well as government funding opportunities (particularly from ARENA).

The commercial and industrial sector is also seeing strong growth. Cost decreases in solar combined with high electricity prices brought on by the energy crisis over the past two years, means that for the first time ever, solar is a cost competitive option compared with traditional electricity contracts for large C&I energy users. In contrast, residential installations peaked in 2012, coinciding with the end of generous feed-in-tariffs and multipliers for small-scale technology certificates (STCs).

Growth in QLD solar is depressing daytime electricity prices

Most in the energy industry are familiar with the duck curve – the hollowing out of daytime electricity demand by solar PV. But solar does not just affect electricity demand. The zero marginal cost of solar means that it is also very good at pushing down daytime electricity prices in the wholesale market.

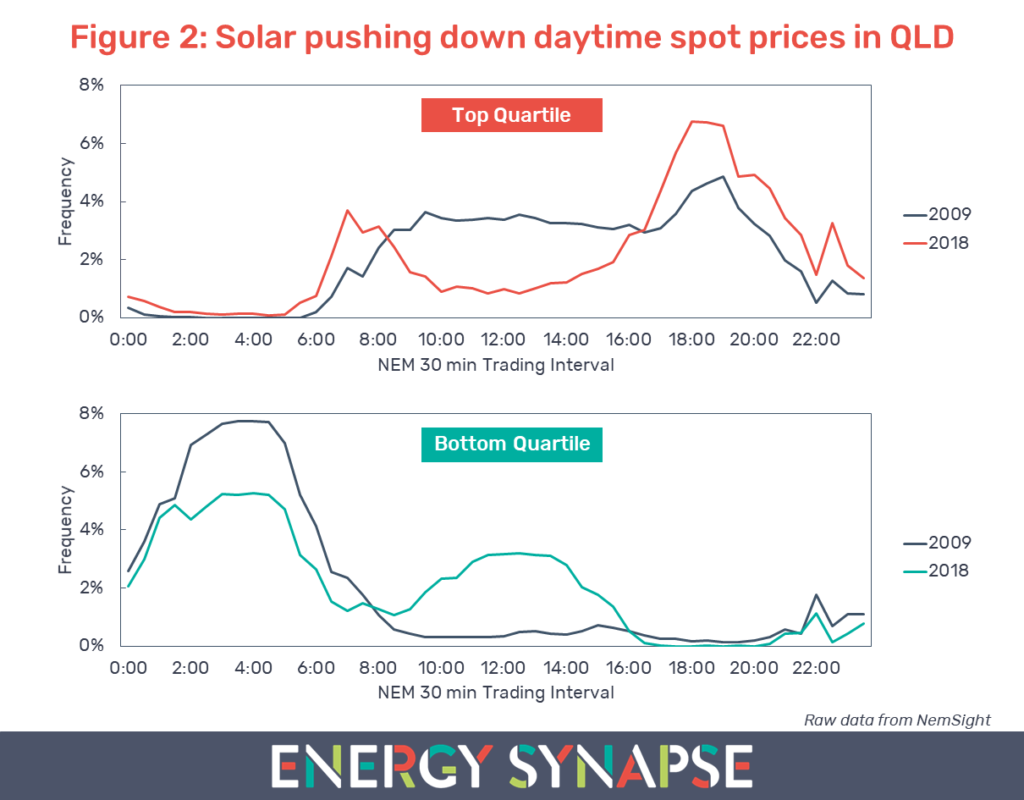

Figure 2 shows how the growth in QLD solar has altered price patterns in the wholesale energy market. The top part of Figure 2 shows the top quartile of spot prices (i.e. top 25% of pricing) in 2009 and 2018. In contrast, the bottom part of Figure 2 shows the bottom quartile (bottom 25% of pricing). We have compiled this data using NemSight, a software developed by Creative Analytics (part of the Energy One group).

Note that Figure 2 shows us how electricity prices in the top and bottom quartile are distributed across each 30 minute Trading Interval. It does not show the value of prices.

We can see that in 2009, the top quartile of pricing was distributed fairly uniformly across daytime trading intervals with a small peak in the evening. The top 25% of prices occurred between 9:00 and 15:30 46% of the time. In contrast, this was only 17% of the time in 2018. High pricing is now occurring more often in the early morning and evening when solar panels are generating little or no power.

Furthermore, these daytime intervals are not only leaving the top quartile of pricing, but are actually entering the bottom quartile. In 2009, the bottom 25% of pricing occurred during 9:00 to 15:30 only 6% of the time. This has increased to 34% in 2018.

The video below shows the full evolution of QLD wholesale electricity prices for the top quartile over the last decade.

Diminishing returns for QLD solar

The big implication of the duck curve in electricity pricing is that those investing in solar may experience diminishing returns. More solar means lower and lower daytime electricity prices. Thus, we may reach a point where electricity prices are so low during the day, that further investment in solar can no longer be justified.

There is a solution to this problem of course, and that is energy storage. Combining solar with storage allows energy to be shifted to more valuable times of the day, thereby increasing revenue for investors. For anyone building QLD solar projects, the question is not if you should add storage, but when.

Want to know how solar and wind farms are performing in the NEM and what revenues they are receiving? Get a copy of our detailed analysis.

Author: Marija Petkovic, Founder & Managing Director of Energy Synapse

Follow Marija on LinkedIn | Twitter